Company grows system size and record development pipeline each by 4%

PARSIPPANY, N.J. (October 22, 2025) – Wyndham Hotels & Resorts (NYSE: WH) today announced results for the three months ended September 30, 2025. Highlights include:

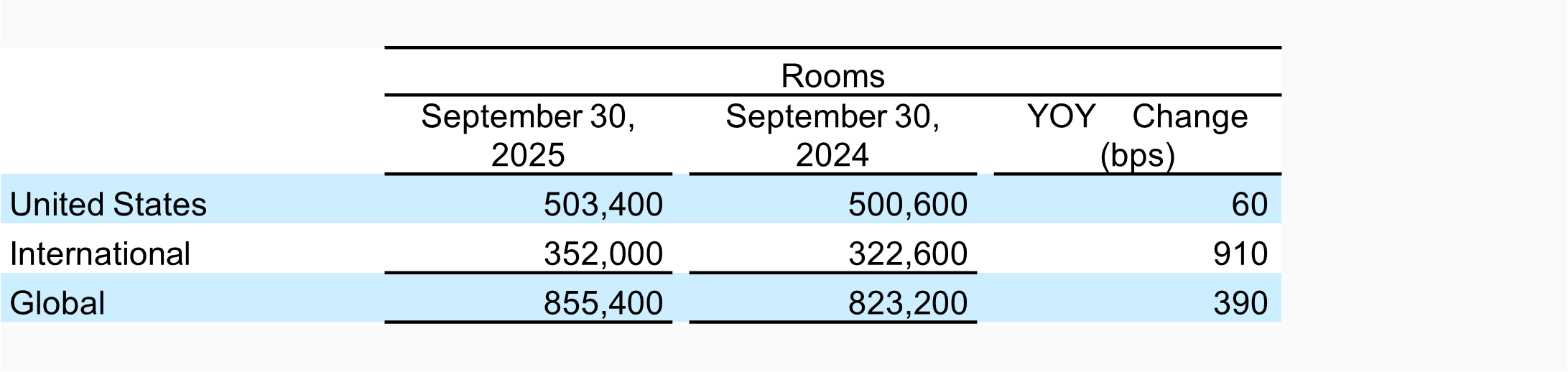

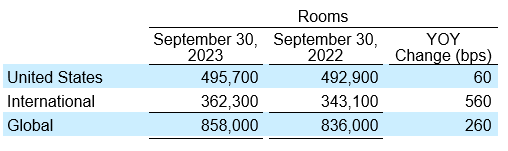

System-wide rooms grew 4% year-over-year.

Awarded 204 development contracts globally, an increase of 24% year-over-year.

Development pipeline grew 4% year-over-year and 1% sequentially to a record 257,000 rooms.

Ancillary revenues increased 18% compared to third quarter 2024 and 14% on a year-to-date basis.

Diluted earnings per share increased 5% year-over-year to $36; adjusted diluted EPS grew 5% to $1.46, or increased 1% on a comparable basis.

Net income increased 3% year-over-year to $105 million; adjusted net income increased 2% to $112 million, or decreased 2% on a comparable basis.

Adjusted EBITDA increased 2% year-over-year to $213 million, or remained flat on a comparable basis.

Returned $101 million to shareholders through $70 million of share repurchases and quarterly cash dividends of $0.41 per share.

“Our third quarter results once again demonstrate the resilience of our business model and the consistent execution of our teams around the world,” said Geoff Ballotti, president and chief executive officer. “Amid a challenging macro backdrop, we delivered record year-to-date organic room openings, grew our global pipeline to another all-time high, and achieved double-digit growth in ancillary revenues – all while expanding our portfolio with high-quality, FeePAR-accretive hotels. As we continue to focus development on our strongest brands and markets, advance the industry’s leading technology and loyalty platforms and drive meaningful returns to shareholders, we’re positioning Wyndham for sustained growth and value creation well into 2026 and beyond.”

Reporting Methodology Beginning in the second quarter of 2025, the Company revised its reporting methodology to exclude the impact of all rooms under the Super 8 China master license agreement from its reported system size, RevPAR and royalty rate, and corresponding growth metrics. The Company’s financial results will continue to reflect fees due from the Super 8 master licensee in China, which contributed less than $3 million to the Company’s full-year 2024 consolidated adjusted EBITDA.

System Size and Development

The Company’s global system grew 4% including 2% growth in the higher RevPAR midscale and above segments in the U.S. and 7% growth in the higher RevPAR EMEA and Latin America regions.

On September 30, 2025, the Company’s pipeline consisted of approximately 2,180 hotels and 257,000 rooms, representing another record-high level and a 4% year-over-year increase. Key highlights include:

Awarded 204 new contracts, an increase of 24% year-over-year.

4% pipeline growth in the U.S. and 4% growth internationally

Approximately 70% of the pipeline is in the midscale and above segments, which grew 4% year-over-year

Approximately 17% of the pipeline is in the extended stay segment

Approximately 58% of the pipeline is international

Approximately 75% of the pipeline is new construction and approximately 36% of these projects have broken ground; rooms under construction grew 3% year-over-year

RevPAR

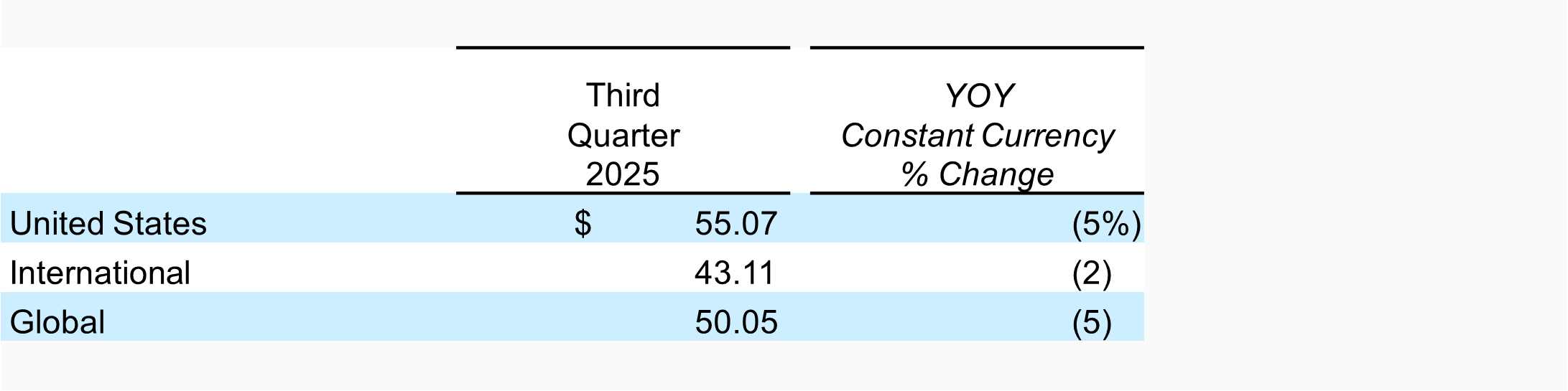

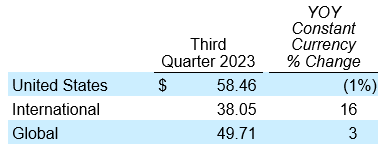

Third quarter global RevPAR decreased 5% in constant currency compared to 2024, reflecting declines of 5% in the U.S. and 2% internationally.

In the U.S., RevPAR performance reflected a 300 basis-point reduction in occupancy and a 200 basis-point decline in ADR. Softer results in Texas, Florida and California were partially offset by continued strength across the Midwest.

Internationally, the decrease was primarily driven by Asia Pacific, including China where RevPAR declined 10%, and Latin America, where RevPAR declined 5%. This was partially offset by 4% growth in the EMEA region and 8% growth in Canada, both primarily reflecting pricing power.

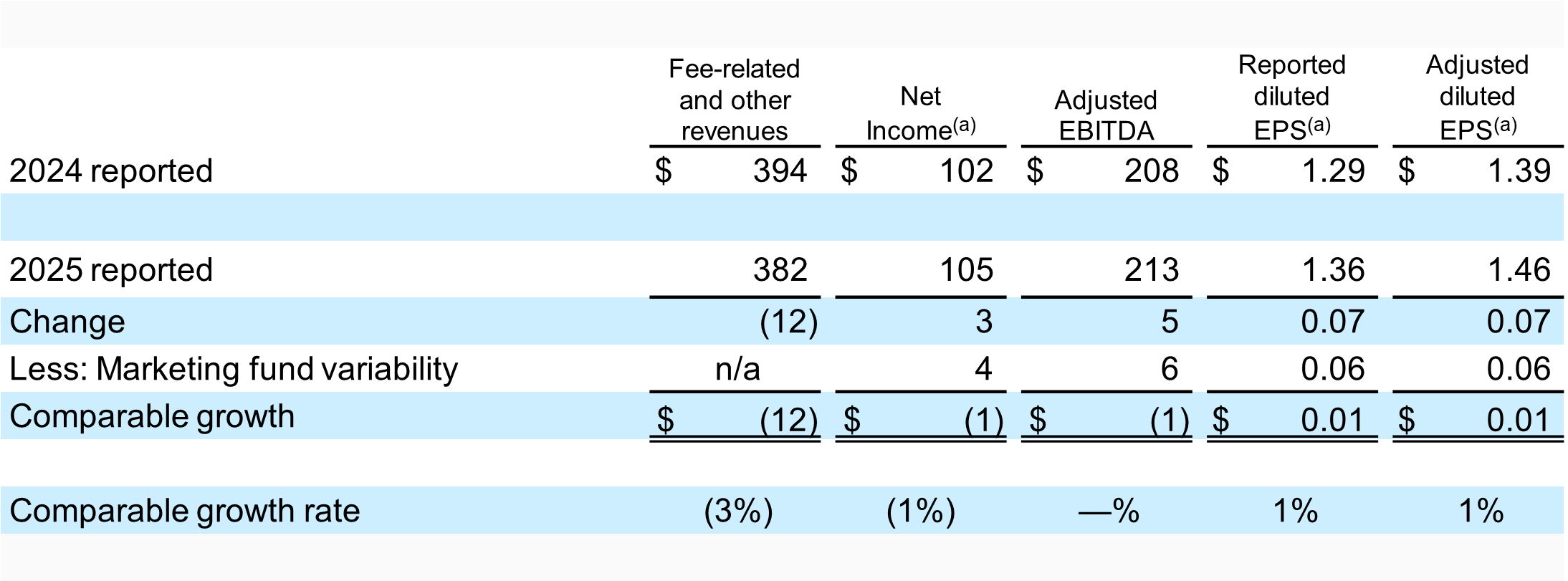

Third Quarter Operating Results The comparability of the Company’s third quarter results is impacted by marketing fund variability. The Company’s reported results and comparable-basis results (adjusted to neutralize these impacts) are presented below to enhance transparency and provide a better understanding of the results of the Company’s ongoing operations.

Fee-related and other revenues were $382 million compared to $394 million in third quarter 2024, reflecting a 5% decline in RevPAR and lower other franchise fees, partially offset by an 18% increase in ancillary revenue, royalty rate expansion both domestically and internationally and global net room growth of 4%.

The Company generated net income of $105 million compared to $102 million in third quarter 2024, primarily due to higher adjusted EBITDA, partially offset by higher interest expense. Adjusted net income was $112 million compared to $110 million in third quarter 2024.

Adjusted EBITDA grew 2% to $213 million compared to $208million in third quarter 2024. This increase included a $6 million favorable impact from marketing fund variability, excluding which adjusted EBITDA remained flat on a comparable basis as lower royalties and franchise fees, along with elevated costs associated with insurance, litigation defense and employee benefits – all of which are reflective of the broader operating environment – were more than offset by cost containment measures, including both operational efficiencies and one-time variable reductions.

Diluted earnings per share increased 5% to $36 compared to $1.29 in third quarter 2024. This increase primarily reflects the benefit of a lower share count due to share repurchase activity.

Adjusted diluted EPS grew 5% to $1.46 compared to $1.39 in third quarter 2024. This increase included a favorable impact of $0.06 per share related to marketing fund variability (after estimated taxes). On a comparable basis, adjusted diluted EPS increased 1% year-over-year primarily reflecting the benefit of share repurchase activity, partially offset by higher interest expense.

During third quarter 2025, the Company’s marketing fund revenues exceeded expenses by $18 million; while in third quarter 2024, the Company’s marketing fund revenues exceeded expenses by $12 million, resulting in $6 million of marketing fund variability.

Full reconciliations of GAAP results to the Company’s non-GAAP adjusted measures for all reported periods appear in the tables to this press release.

Balance Sheet and Liquidity The Company generated $86 million of net cash provided by operating activities and $97 million of free cash flow in third quarter 2025. The Company ended the quarter with a cash balance of $70 million and approximately $540 million in total liquidity.

The Company’s net debt leverage ratio was 3.5 times at September 30, 2025, the midpoint of the Company’s 3 to 4 times stated target range and in line with expectations.

In October 2025, the Company refinanced its $750 million revolving credit facility, extending the maturity from April 2027 to October 2030, increasing capacity by $250 million to $1 billion, and reducing borrowing costs by 35 basis points. All other terms remain similar to the previous facility.

Share Repurchases and Dividends During the third quarter, the Company repurchased approximately 830,000 shares of its common stock for $70 million. Year-to-date through September 30, the Company repurchased approximately 2.5 million shares of its common stock for $223 million.

The Company paid common stock dividends of $31 million, or $0.41 per share, during the third quarter 2025.

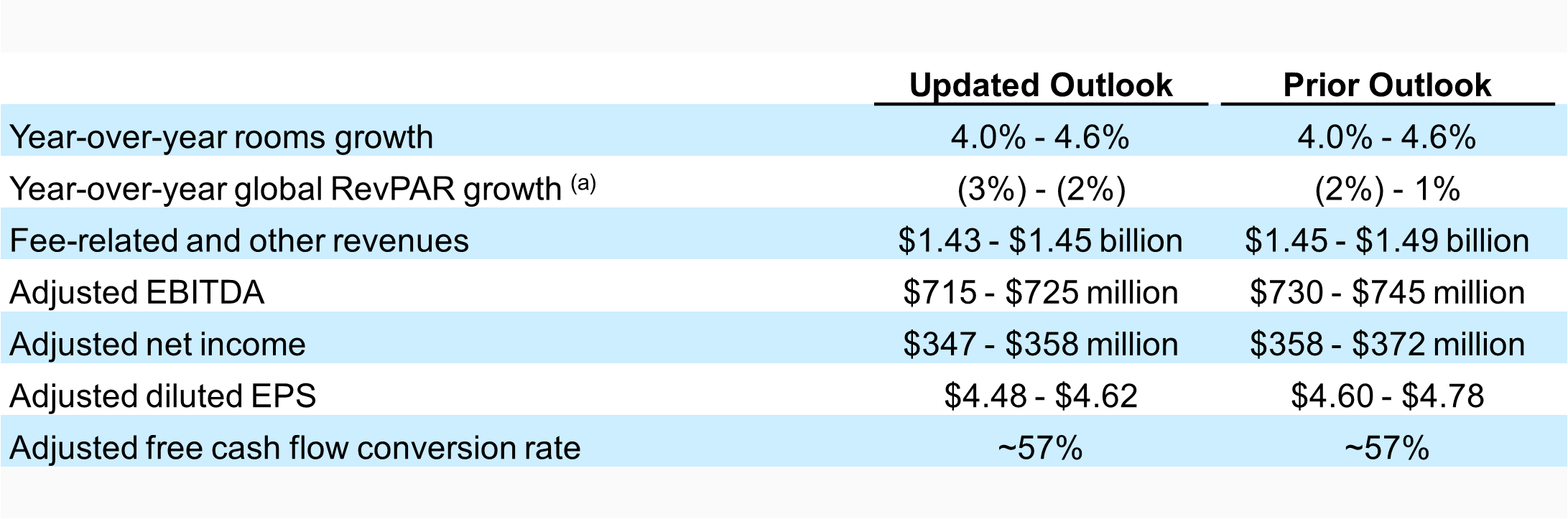

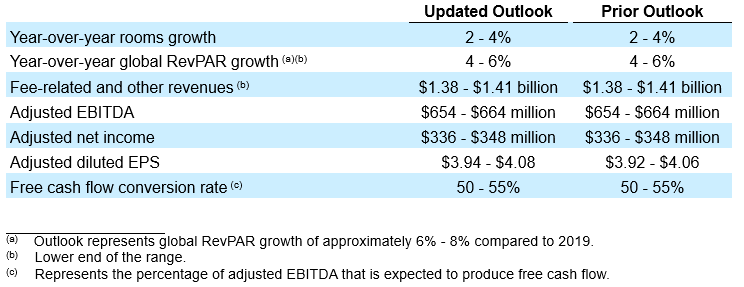

Full-Year 2025 Outlook The Company is updating its full-year outlook as follows: The Company expects marketing fund expenses to exceed revenues by approximately $5 million during full-year 2025, an intentional investment the Company expects to recover in future periods.

More detailed projections are available in Table 8 of this press release. The Company is providing certain financial metrics only on a non-GAAP basis because, without unreasonable efforts, it is unable to predict with reasonable certainty the occurrence or amount of all of the adjustments or other potential adjustments that may arise in the future during the forward-looking period, which can be dependent on future events that may not be reliably predicted. Based on past reported results, where one or more of these items have been applicable, such excluded items could be material, individually or in the aggregate, to the reported results.

Conference Call Information Wyndham Hotels will hold a conference call with investors to discuss the Company’s results and outlook on Thursday, October 23, 2025 at 8:30 a.m. ET. Listeners can access the webcast live through the Company’s website at https://investor.wyndhamhotels.com. The conference call may also be accessed by dialing 800 343-4136 and providing the passcode “Wyndham”. Listeners are urged to call at least five minutes prior to the scheduled start time. An archive of this webcast will be available on the website beginning at noon ET on October 23, 2025. A telephone replay will be available for approximately ten days beginning at noon ET on October 23, 2025 at 800 939-8292.

Presentation of Financial Information Financial information discussed in this press release includes non-GAAP measures, which include or exclude certain items. These non-GAAP measures differ from reported GAAP results and are intended to illustrate what management believes are relevant period-over-period comparisons and are helpful to investors as an additional tool for further understanding and assessing the Company’s ongoing operating performance. The Company uses these measures internally to assess its operating performance, both absolutely and in comparison to other companies, and to make day to day operating decisions, including in the evaluation of selected compensation decisions. Exclusion of items in the Company’s non-GAAP presentation should not be considered an inference that these items are unusual, infrequent or non-recurring. Full reconciliations of GAAP results to the comparable non-GAAP measures for the reported periods appear in the financial tables section of this press release.

About Wyndham Hotels & Resorts Wyndham Hotels & Resorts (NYSE: WH) is the world’s largest hotel franchising company by the number of franchised properties, with approximately 8,300 hotels across approximately 100 countries on six continents. Through its network of over 855,000 rooms appealing to the everyday traveler, Wyndham commands a leading presence in the economy and midscale segments of the lodging industry. The Company operates a portfolio of 25 hotel brands, including Super 8®, Days Inn®, Ramada®, Microtel®, La Quinta®, Baymont®, Wingate®, AmericInn®, ECHO Suites®, Registry Collection Hotels®, Trademark Collection® and Wyndham®. The Company’s award-winning Wyndham Rewards loyalty program offers approximately 121 million enrolled members the opportunity to redeem points at thousands of hotels, vacation club resorts and vacation rentals globally. For more information, visit https://investor.wyndhamhotels.com. The Company may use its website and social media channels as means of disclosing material non-public information and for complying with its disclosure obligations under Regulation FD. Disclosures of this nature will be included on the Company’s website in the Investors section, which can currently be accessed at https://investor.wyndhamhotels.com or on the Company’s social media channels, including the Company’s LinkedIn account which can currently be accessed at https://www.linkedin.com/company/wyndhamhotels. Accordingly, investors should monitor this section of the Company’s website and the Company’s social media channels in addition to following the Company’s press releases, filings submitted with the Securities and Exchange Commission and any public conference calls or webcasts.

Forward-Looking Statements This press release contains “forward-looking statements” within the meaning of the federal securities laws, including statements related to Wyndham’s current views and expectations with respect to its future performance and operations, including revenues, earnings, cash flow and other financial and operating measures, share repurchases and dividends and restructuring charges. Forward-looking statements are any statements other than statements of historical fact, including those that convey management’s expectations as to the future based on plans, estimates and projections at the time Wyndham makes the statements and may be identified by words such as “will,” “expect,” “believe,” “plan,” “anticipate,” “predict,” “intend,” “goal,” “future,” “forward,” “remain,” “confident,” “outlook,” “guidance,” “target,” “objective,” “estimate,” “projection” and similar words or expressions, including the negative version of such words and expressions. Such forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause the actual results, performance or achievements of Wyndham to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press release.

Factors that could cause actual results to differ materially from those in the forward-looking statements include, without limitation, general economic conditions, including inflation, higher interest rates and potential recessionary pressures, which may impact decisions by consumers and businesses to use travel accommodations; global trade disputes, including with China; the performance of the financial and credit markets; the economic environment for the hospitality industry; operating risks associated with the hotel franchising business; Wyndham’s relationships with franchisees; the ability of franchisees to pay back loans owed to Wyndham; the impact of war, terrorist activity, political instability or political strife, including the ongoing conflicts between Russia and Ukraine and conflicts in the Middle East, respectively; global or regional health crises or pandemics including the resulting impact on Wyndham’s business, operations, financial results, cash flows and liquidity, as well as the impact on its franchisees, guests and team members, the hospitality industry and overall demand for and restrictions on travel; Wyndham’s ability to satisfy obligations and agreements under its outstanding indebtedness, including the payment of principal and interest and compliance with the covenants thereunder; risks related to Wyndham’s ability to obtain financing and the terms of such financing, including access to liquidity and capital; and Wyndham’s ability to make or pay, plans for and the timing and amount of any future share repurchases and/or dividends, as well as the risks described in Wyndham’s most recent Annual Report on Form 10-K filed with the Securities and Exchange Commission and any subsequent reports filed with the Securities and Exchange Commission. These risks and uncertainties are not the only ones Wyndham may face and additional risks may arise or become material in the future. Wyndham undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, subsequent events or otherwise, except as required by law.

Company Raises Full-Year 2025 EPS Outlook

Grows Development Pipeline by 5% and System Size by 4%

PARSIPPANY, N.J. (July 23, 2025) – Wyndham Hotels & Resorts (NYSE: WH) today announced results for the three months ended June 30, 2025. Highlights include:

System-wide rooms grew 4% year-over-year.

Awarded 229 development contracts globally, an increase of 40% year-over-year.

Development pipeline grew 1% sequentially and 5% year-over-year to a record 255,000 rooms.

Ancillary revenues increased 19% compared to second quarter 2024 and 13% on a year-to date basis.

Diluted earnings per share increased 6% year-over-year to $13; adjusted diluted EPS grew 18% to $1.33, or 11% on a comparable basis.

Net income increased 1% year-over-year to $87 million; adjusted net income increased 13% to $103 million, or 7% on a comparable basis.

Adjusted EBITDA increased 10% year-over-year to $195 million, or 5% on a comparable basis.

Returned $109 million to shareholders through $77 million of share repurchases and quarterly cash dividends of $0.41 per share.

“We delivered another solid quarter growing our global system by 4%, expanding our development pipeline by 5%, increasing our ancillary revenues by 19%, and continuing to execute our strategy focused on higher FeePAR segments and markets, which is driving growth in both domestic and international royalty rates,” said Geoff Ballotti, president and chief executive officer. “Record first-half openings and a 40% second quarter increase in new contracts awarded reflect strong developer confidence in Wyndham’s powerful, owner-first value proposition. Amid a softer domestic RevPAR environment, we grew comparable adjusted EBITDA by 5% and comparable adjusted EPS by 11%. We also returned nearly $110 million to shareholders this quarter — continuing to demonstrate the value-creating power of our highly cash-generative, resilient asset-light business model. With consistent development, royalty rate, and ancillary fee growth, we remain very confident in our ability to create long-term value for our shareholders, franchisees, and team members through the enduring appeal of our iconic brands.”

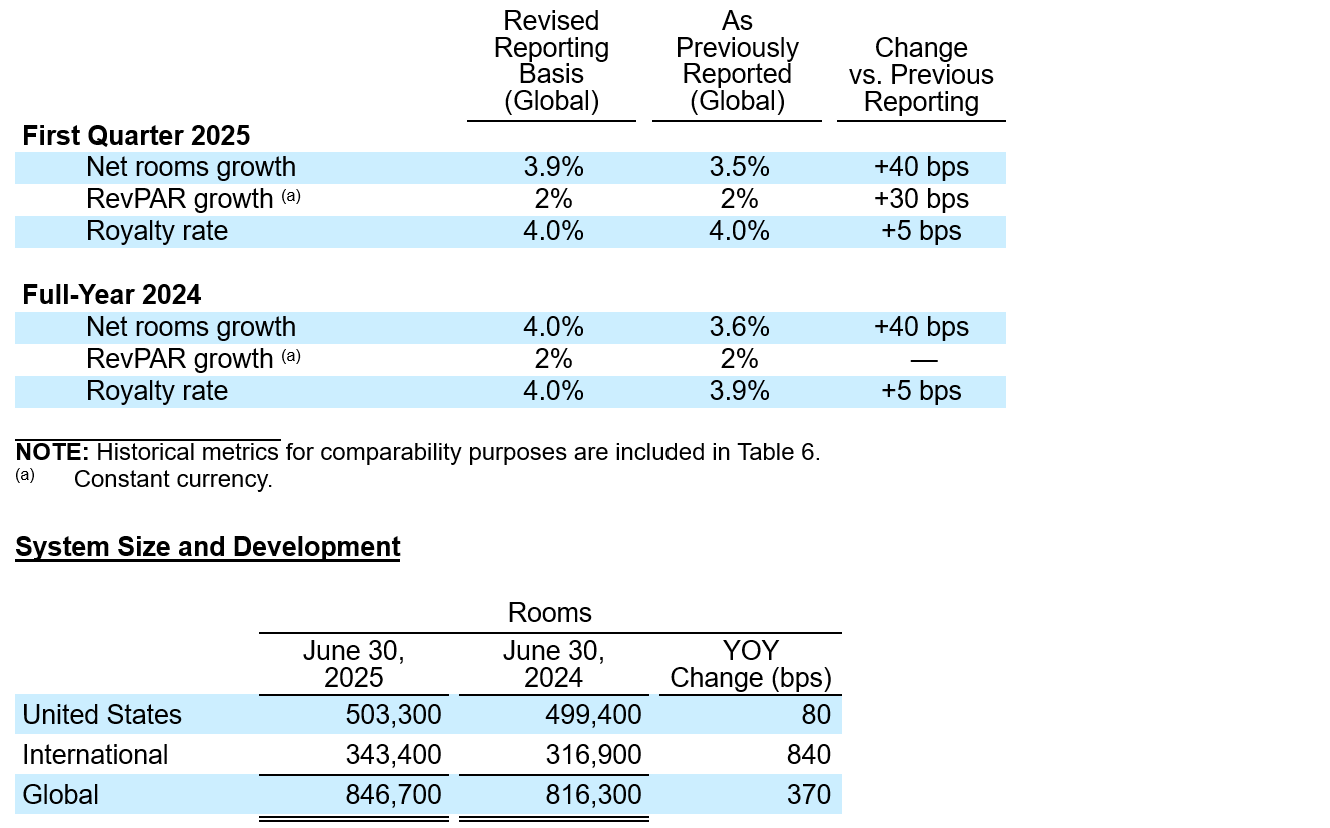

Revised International Reporting Basis As part of a recent operational review, the Company identified violations of its Super 8 master license agreement in China and issued a notice of default to the master licensee. Given the operational challenges of obtaining accurate information from this master licensee and the uncertain outcome of the compliance process, beginning this quarter, the Company has revised its reporting methodology to exclude the impact of all rooms (approximately 67,300 rooms as of March 31, 2025) under this master license agreement from its reported system size, RevPAR and royalty rate, and corresponding growth metrics. The Company’s financial results will continue to reflect fees due from the Super 8 master licensee in China, which contributed less than $3 million to the Company’s full-year 2024 consolidated adjusted EBITDA.

To provide further context, the following table reflects the impact on the Company’s global growth metrics as a result of the exclusion of its Super 8 master license agreement in China:

The Company’s global system grew 4% including 3% growth in the higher RevPAR midscale and above segments in the U.S. and 5% growth in the higher RevPAR EMEA and Latin America regions.

On June 30, 2025, the Company’s pipeline consisted of approximately 2,150 hotels and 255,000 rooms, representing another record-high level and a 5% year-over-year increase. Key highlights include:

Awarded 229 new contracts, an increase of 40% year-over-year.

6% pipeline growth in the U.S. and 4% growth internationally

Approximately 70% of the pipeline is in the midscale and above segments, which grew 5% year-over-year

Approximately 17% of the pipeline is in the extended stay segment

Approximately 58% of the pipeline is international

Approximately 76% of the pipeline is new construction and approximately 35% of these projects have broken ground

RevPAR

Second quarter global RevPAR decreased 3% in constant currency compared to 2024, reflecting a 4% decline in the U.S. and 1% growth internationally.

In the U.S., second quarter results included approximately 150 basis points of unfavorable impacts from the timing of the Easter holiday and the 2024 solar eclipse. Excluding these impacts, the Company’s U.S. RevPAR declined approximately 2.3% year-over-year, driven by softer demand, partially offset by a modest increase in pricing.

Internationally, RevPAR results were driven by continued pricing power, offset by a decline in occupancy. The Company continued to see strong performance in its EMEA and Latin America regions, with year-over-year growth of 7% and 18%, respectively, reflecting robust pricing power in both regions. The Company’s Canada region grew RevPAR by 7% reflecting increased room nights from Canadian guests. In China, RevPAR decreased 8% year-over-year reflecting a decline in occupancy and continued pricing pressure.

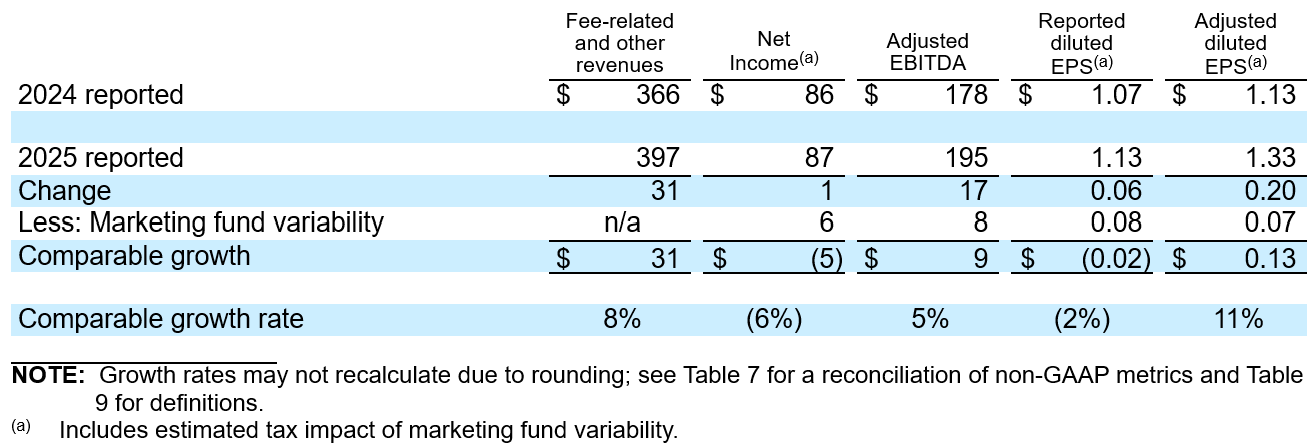

Second Quarter Operating Results The comparability of the Company’s second quarter results is impacted by marketing fund variability. The Company’s reported results and comparable-basis results (adjusted to neutralize these impacts) are presented below to enhance transparency and provide a better understanding of the results of the Company’s ongoing operations.

Fee-related and other revenues grew 8% to $397 million compared to $366 million in second quarter 2024, which reflects a 19% increase in ancillary revenues, higher royalties and franchise fees, as well as higher pass-through revenues due to the Company’s global franchisee conference in May.

The Company generated net income of $87 million, a 1% increase compared to second quarter 2024, as higher adjusted EBITDA and lower transaction-related expenses were partially offset by the absence of a benefit in connection with the reversal of a spin-off related matter, higher restructuring costs, and increased interest expense. Adjusted net income grew 13% to $103 million compared to $91 million in second quarter 2024.

Adjusted EBITDA grew 10% to $195 million compared to $178million in second quarter 2024. This increase included an $8 million favorable impact from marketing fund variability, excluding which adjusted EBITDA grew 5% on a comparable basis, primarily reflecting increased ancillary revenues, as well as higher royalties and franchise fees, partially offset by higher operating expenses primarily related to growth in the Company’s credit card program and the absence of a benefit from insurance recoveries.

Diluted earnings per share increased 6% to $13 compared to $1.07 in second quarter 2024. This increase primarily reflects the benefit of a lower share count due to share repurchase activity.

Adjusted diluted EPS grew 18% to $1.33 compared to $1.13 in second quarter 2024. This increase included a favorable impact of $0.07 per share related to marketing fund variability (after estimated taxes). On a comparable basis, adjusted diluted EPS increased approximately 11% year-over-year, reflecting comparable adjusted EBITDA growth, the benefit of share repurchase activity and lower depreciation and amortization, partially offset by higher interest expense.

During second quarter 2025, the Company’s marketing fund revenues exceeded expenses by $3 million; while in second quarter 2024, the Company’s marketing fund expenses exceeded revenues by $5 million, resulting in $8 million of marketing fund variability.

Full reconciliations of GAAP results to the Company’s non-GAAP adjusted measures for all reported periods appear in the tables to this press release.

Balance Sheet and Liquidity The Company generated $70 million of net cash provided by operating activities and $88 million of adjusted free cash flow in second quarter 2025. The Company ended the quarter with a cash balance of $50 million and approximately $580 million in total liquidity.

The Company’s net debt leverage ratio was 3.5 times at June 30, 2025, the midpoint of the Company’s 3 to 4 times stated target range and in line with expectations.

Share Repurchases and Dividends During the second quarter, the Company repurchased approximately 923,000 shares of its common stock for $77 million.

The Company paid common stock dividends of $32 million, or $0.41 per share, during the second quarter 2025.

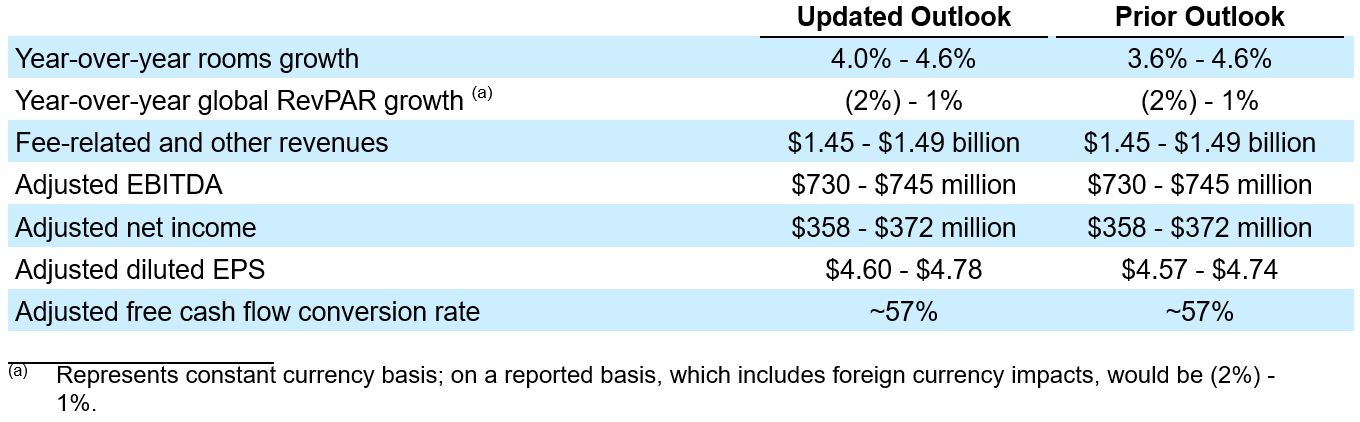

Full-Year 2025 Outlook The Company is increasing its adjusted diluted EPS outlook to reflect the impact of second quarter share repurchase activity and increasing the low-end of its year-over-year rooms growth outlook by 40 basis points to reflect the removal of the dilutive impact from its Super 8 master licensee in China.

The Company continues to expect marketing fund revenues to approximate expenses during full-year 2025 though seasonality of spend will affect the quarterly comparisons throughout the year.

More detailed projections are available in Table 8 of this press release. The Company is providing certain financial metrics only on a non-GAAP basis because, without unreasonable efforts, it is unable to predict with reasonable certainty the occurrence or amount of all of the adjustments or other potential adjustments that may arise in the future during the forward-looking period, which can be dependent on future events that may not be reliably predicted. Based on past reported results, where one or more of these items have been applicable, such excluded items could be material, individually or in the aggregate, to the reported results.

Conference Call Information Wyndham Hotels will hold a conference call with investors to discuss the Company’s results and outlook on Thursday, July 24, 2025 at 8:30 a.m. ET. Listeners can access the webcast live through the Company’s website at https://investor.wyndhamhotels.com. The conference call may also be accessed by dialing 800 343-4136 and providing the passcode “Wyndham”. Listeners are urged to call at least five minutes prior to the scheduled start time. An archive of this webcast will be available on the website beginning at noon ET on July 24, 2025. A telephone replay will be available for approximately ten days beginning at noon ET on July 24, 2025 at 800 723-8184.

Presentation of Financial Information Financial information discussed in this press release includes non-GAAP measures, which include or exclude certain items. These non-GAAP measures differ from reported GAAP results and are intended to illustrate what management believes are relevant period-over-period comparisons and are helpful to investors as an additional tool for further understanding and assessing the Company’s ongoing operating performance. The Company uses these measures internally to assess its operating performance, both absolutely and in comparison to other companies, and to make day to day operating decisions, including in the evaluation of selected compensation decisions. Exclusion of items in the Company’s non-GAAP presentation should not be considered an inference that these items are unusual, infrequent or non-recurring. Full reconciliations of GAAP results to the comparable non-GAAP measures for the reported periods appear in the financial tables section of this press release.

About Wyndham Hotels & Resorts Wyndham Hotels & Resorts (NYSE: WH) is the world’s largest hotel franchising company by the number of franchised properties, with approximately 8,300 hotels across approximately 100 countries on six continents. Through its network of approximately 847,000 rooms appealing to the everyday traveler, Wyndham commands a leading presence in the economy and midscale segments of the lodging industry. The Company operates a portfolio of 25 hotel brands, including Super 8®, Days Inn®, Ramada®, Microtel®, La Quinta®, Baymont®, Wingate®, AmericInn®, ECHO Suites®, Registry Collection Hotels®, Trademark Collection® and Wyndham®. The Company’s award-winning Wyndham Rewards loyalty program offers approximately 120 million enrolled members the opportunity to redeem points at thousands of hotels, vacation club resorts and vacation rentals globally. For more information, visit https://investor.wyndhamhotels.com. The Company may use its website and social media channels as means of disclosing material non-public information and for complying with its disclosure obligations under Regulation FD. Disclosures of this nature will be included on the Company’s website in the Investors section, which can currently be accessed at https://investor.wyndhamhotels.com or on the Company’s social media channels, including the Company’s LinkedIn account which can currently be accessed at https://www.linkedin.com/company/wyndhamhotels. Accordingly, investors should monitor this section of the Company’s website and the Company’s social media channels in addition to following the Company’s press releases, filings submitted with the Securities and Exchange Commission and any public conference calls or webcasts.

Forward-Looking Statements This press release contains “forward-looking statements” within the meaning of the federal securities laws, including statements related to Wyndham’s current views and expectations with respect to its future performance and operations, including revenues, earnings, cash flow and other financial and operating measures, share repurchases and dividends and restructuring charges. Forward-looking statements are any statements other than statements of historical fact, including those that convey management’s expectations as to the future based on plans, estimates and projections at the time Wyndham makes the statements and may be identified by words such as “will,” “expect,” “believe,” “plan,” “anticipate,” “predict,” “intend,” “goal,” “future,” “forward,” “remain,” “confident,” “outlook,” “guidance,” “target,” “objective,” “estimate,” “projection” and similar words or expressions, including the negative version of such words and expressions. Such forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause the actual results, performance or achievements of Wyndham to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press release.

Factors that could cause actual results to differ materially from those in the forward-looking statements include, without limitation, general economic conditions, including inflation, higher interest rates and potential recessionary pressures, which may impact decisions by consumers and businesses to use travel accommodations; global trade disputes, including with China; the performance of the financial and credit markets; the economic environment for the hospitality industry; operating risks associated with the hotel franchising business; Wyndham’s relationships with franchisees; the impact of war, terrorist activity, political instability or political strife, including the ongoing conflicts between Russia and Ukraine and conflicts in the Middle East, respectively; global or regional health crises or pandemics including the resulting impact on Wyndham’s business, operations, financial results, cash flows and liquidity, as well as the impact on its franchisees, guests and team members, the hospitality industry and overall demand for and restrictions on travel; Wyndham’s ability to satisfy obligations and agreements under its outstanding indebtedness, including the payment of principal and interest and compliance with the covenants thereunder; risks related to Wyndham’s ability to obtain financing and the terms of such financing, including access to liquidity and capital; and Wyndham’s ability to make or pay, plans for and the timing and amount of any future share repurchases and/or dividends, as well as the risks described in Wyndham’s most recent Annual Report on Form 10-K filed with the Securities and Exchange Commission and any subsequent reports filed with the Securities and Exchange Commission. These risks and uncertainties are not the only ones Wyndham may face and additional risks may arise or become material in the future. Wyndham undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, subsequent events or otherwise, except as required by law.

Company Delivers Record First Quarter Openings and Development Pipeline

PARSIPPANY, N.J. (April 30, 2025) – Wyndham Hotels & Resorts (NYSE: WH) today announced results for the three months ended March 31, 2025. Highlights include:

Global openings of 15,000 rooms increased 13% year-over-year, a record first quarter.

System-wide rooms grew 4% year-over-year.

Awarded 181 development contracts globally, an increase of 6% year-over-year.

Development pipeline grew 1% sequentially and 5% year-over-year to a record 254,000 rooms.

Global RevPAR grew 2% in constant currency.

Fee-related and other revenues increased 4% year-over-year.

Diluted earnings per share of $78 compared to $0.19 in the prior-year quarter and adjusted diluted EPS grew 10% year-over-year to $0.86, or 20% on a comparable basis.

Net income of $61 million compared to $16 million in the prior-year quarter; adjusted net income increased 5% year-over-year to $67 million, or 14% on a comparable basis.

Adjusted EBITDA increased 3% year-over-year to $145 million, or 9% on a comparable basis.

Returned $109 million to shareholders through $76million of share repurchases and quarterly cash dividends of $0.41 per share.

“We delivered a solid start to the year with strong system growth, record first-quarter openings and continued expansion across every region,” said Geoff Ballotti, president and chief executive officer. “While the macro environment remains uncertain, we’re staying focused on what we can control — investing in high-quality growth, executing with discipline and supporting our franchisees. Our asset-light, franchise-only business model has consistently outperformed during economic downturns and positions us well to deliver long-term value for our shareholders through all phases of any economic cycle.”

System Size and Development

The Company’s global system grew 4%. Importantly, these results included 4% growth in the higher RevPAR midscale and above segments in the U.S., as well as strong growth in the Company’s higher RevPAR EMEA and Latin America regions, which grew a combined 6%. The Company remains on track to achieve its net room growth outlook of 3.6% to 4.6% for the full year 2025.

On March 31, 2025, the Company’s global development pipeline consisted of approximately 2,140 hotels and 254,000 rooms, representing another record-high level and a 5% year-over-year increase. Key highlights include:

5% growth in the U.S. and 4% internationally

19th consecutive quarter of sequential pipeline growth

Approximately 70% of the pipeline is in the midscale and above segments, which grew 7% year-over-year

Approximately 17% of the pipeline is in the extended stay segment

Approximately 58% of the pipeline is international

Approximately 77% of the pipeline is new construction and approximately 35% of these projects have broken ground

During first quarter 2025, the Company awarded 181 new contracts, an increase of 6% year-over-year.

RevPAR

First quarter global RevPAR increased 2% in constant currency compared to 2024, reflecting 2% growth in the U.S. and 3% growth internationally.

In the U.S., RevPAR growth includes 100 basis points of benefit from hurricanes and the timing of the Easter holiday. Excluding those factors, the Company’s U.S. RevPAR grew 60 basis points year-over-year as pricing strength was partially offset by softer demand with the pullback more pronounced during March.

Internationally, RevPAR growth was also driven by pricing power. The Company continued to see strong performance in its EMEA and Latin America regions, with year-over-year growth of 6% and 25%, respectively, reflecting robust pricing power, partially offset by modest occupancy declines. In China, demand remained steady but RevPAR declined 8% year-over-year reflecting continued pricing pressure.

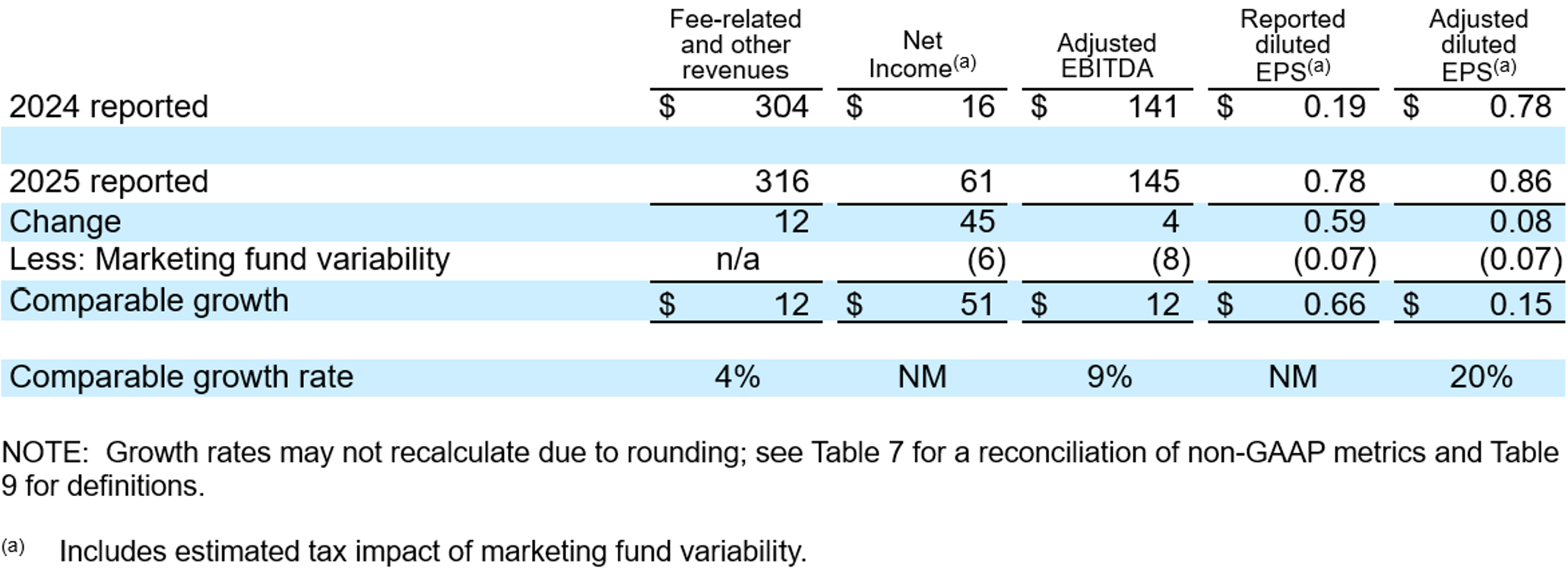

First Quarter Operating Results The comparability of the Company’s first quarter results is impacted by marketing fund variability. The Company’s reported results and comparable-basis results (adjusted to neutralize these impacts) are presented below to enhance transparency and provide a better understanding of the results of the Company’s ongoing operations.

Fee-related and other revenues grew 4% to $316 million compared to $304 million in first quarter 2024, which reflects higher royalties and franchise fees and higher ancillary revenues.

The Company generated net income of $61 million compared to $16 million in first quarter 2024. The increase primarily reflects lower transaction-related expenses in connection with defending an unsuccessful hostile takeover attempt. Other items primarily include the absence of impairment and restructuring costs recorded in first quarter 2024, partially offset by higher interest expense. Adjusted net income grew 5% to $67 million compared to $64 million in first quarter 2024.

Adjusted EBITDA grew 3% to $145 million compared to $141million in first quarter 2024. This increase included an $8 million unfavorable impact from marketing fund variability, excluding which adjusted EBITDA grew 9% on a comparable basis, primarily reflecting higher fee-related revenues and margin expansion.

Diluted earnings per share was $78 compared to $0.19 in first quarter 2024. This increase reflects higher net income and the benefit of a lower share count due to share repurchase activity.

Adjusted diluted EPS grew 10% to $0.86 compared to $0.78 in first quarter 2024. This increase included an unfavorable impact of $0.07 per share related to marketing fund variability (after estimated taxes). On a comparable basis, adjusted diluted EPS increased approximately 20% year-over-year, reflecting comparable adjusted EBITDA growth, lower depreciation and amortization and the benefit of share repurchase activity, partially offset by higher interest expense.

During first quarter 2025, the Company’s marketing fund expenses exceeded revenues by $22 million; while in first quarter 2024, the Company’s marketing fund expenses exceeded revenues by $14 million, resulting in $8 million of marketing fund variability.

Full reconciliations of GAAP results to the Company’s non-GAAP adjusted measures for all reported periods appear in the tables to this press release.

Balance Sheet and Liquidity The Company generated $59 million of net cash provided by operating activities and $80 million of free cash flow in first quarter 2025. The Company ended the quarter with a cash balance of $48 million and approximately $637 million in total liquidity.

The Company’s net debt leverage ratio was 3.5 times at March 31, 2025, at the midpoint of the Company’s 3 to 4 times stated target range and in line with expectations.

Share Repurchases and Dividends During the first quarter, the Company repurchased approximately 797,000 shares of its common stock for $76 million.

The Company paid common stock dividends of $33 million, or $0.41 per share, during the first quarter 2025.

Full-Year 2025 Outlook The Company is refining its outlook to reflect a softer-than-expected RevPAR environment. The updated range reflects a variety of potential outcomes for the remainder of the year, from a more optimistic scenario in which the softness seen in March and April proves to be temporary, to a more cautious view that contemplates persistent pressure on demand throughout the remainder of the year.

The Company continues to expect marketing fund revenues to approximate expenses during full-year 2025 though seasonality of spend will affect the quarterly comparisons throughout the year.

More detailed projections are available in Table 8 of this press release. The Company is providing certain financial metrics only on a non-GAAP basis because, without unreasonable efforts, it is unable to predict with reasonable certainty the occurrence or amount of all of the adjustments or other potential adjustments that may arise in the future during the forward-looking period, which can be dependent on future events that may not be reliably predicted. Based on past reported results, where one or more of these items have been applicable, such excluded items could be material, individually or in the aggregate, to the reported results.

Conference Call Information Wyndham Hotels will hold a conference call with investors to discuss the Company’s results and outlook on Thursday, May 1, 2025 at 8:30 a.m. ET. Listeners can access the webcast live through the Company’s website at https://investor.wyndhamhotels.com. The conference call may also be accessed by dialing 800 343-4136 and providing the passcode “Wyndham”. Listeners are urged to call at least five minutes prior to the scheduled start time. An archive of this webcast will be available on the website beginning at noon ET on May 1, 2025. A telephone replay will be available for approximately ten days beginning at noon ET on May 1, 2025 at 800 688-9459.

Presentation of Financial Information Financial information discussed in this press release includes non-GAAP measures, which include or exclude certain items. These non-GAAP measures differ from reported GAAP results and are intended to illustrate what management believes are relevant period-over-period comparisons and are helpful to investors as an additional tool for further understanding and assessing the Company’s ongoing operating performance. The Company uses these measures internally to assess its operating performance, both absolutely and in comparison to other companies, and to make day to day operating decisions, including in the evaluation of selected compensation decisions. Exclusion of items in the Company’s non-GAAP presentation should not be considered an inference that these items are unusual, infrequent or non-recurring. Full reconciliations of GAAP results to the comparable non-GAAP measures for the reported periods appear in the financial tables section of this press release.

About Wyndham Hotels & Resorts Wyndham Hotels & Resorts (NYSE: WH) is the world’s largest hotel franchising company by the number of franchised properties, with approximately 9,300 hotels across over 95 countries on six continents. Through its network of approximately 907,000 rooms appealing to the everyday traveler, Wyndham commands a leading presence in the economy and midscale segments of the lodging industry. The Company operates a portfolio of 25 hotel brands, including Super 8®, Days Inn®, Ramada®, Microtel®, La Quinta®, Baymont®, Wingate®, AmericInn®, ECHO Suites®, Registry Collection Hotels®, Trademark Collection® and Wyndham®. The Company’s award-winning Wyndham Rewards loyalty program offers over 115 million enrolled members the opportunity to redeem points at thousands of hotels, vacation club resorts and vacation rentals globally. For more information, visit https://investor.wyndhamhotels.com. The Company may use its website and social media channels as means of disclosing material non-public information and for complying with its disclosure obligations under Regulation FD. Disclosures of this nature will be included on the Company’s website in the Investors section, which can currently be accessed at https://investor.wyndhamhotels.com or on the Company’s social media channels, including the Company’s LinkedIn account which can currently be accessed at https://www.linkedin.com/company/wyndhamhotels. Accordingly, investors should monitor this section of the Company’s website and the Company’s social media channels in addition to following the Company’s press releases, filings submitted with the Securities and Exchange Commission and any public conference calls or webcasts.

Forward-Looking Statements This press release contains “forward-looking statements” within the meaning of the federal securities laws, including statements related to Wyndham’s current views and expectations with respect to its future performance and operations, including revenues, earnings, cash flow and other financial and operating measures, share repurchases and dividends and restructuring charges. Forward-looking statements are any statements other than statements of historical fact, including those that convey management’s expectations as to the future based on plans, estimates and projections at the time Wyndham makes the statements and may be identified by words such as “will,” “expect,” “believe,” “plan,” “anticipate,” “predict,” “intend,” “goal,” “future,” “forward,” “remain,” “confident,” “outlook,” “guidance,” “target,” “objective,” “estimate,” “projection” and similar words or expressions, including the negative version of such words and expressions. Such forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause the actual results, performance or achievements of Wyndham to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press release.

Factors that could cause actual results to differ materially from those in the forward-looking statements include, without limitation, general economic conditions, including inflation, higher interest rates and potential recessionary pressures, which may impact decisions by consumers and businesses to use travel accommodations; global trade disputes, including with China; the performance of the financial and credit markets; the economic environment for the hospitality industry; operating risks associated with the hotel franchising business; Wyndham’s relationships with franchisees; the impact of war, terrorist activity, political instability or political strife, including the ongoing conflicts between Russia and Ukraine and conflicts in the Middle East, respectively; global or regional health crises or pandemics including the resulting impact on Wyndham’s business, operations, financial results, cash flows and liquidity, as well as the impact on its franchisees, guests and team members, the hospitality industry and overall demand for and restrictions on travel; Wyndham’s ability to satisfy obligations and agreements under its outstanding indebtedness, including the payment of principal and interest and compliance with the covenants thereunder; risks related to Wyndham’s ability to obtain financing and the terms of such financing, including access to liquidity and capital; and Wyndham’s ability to make or pay, plans for and the timing and amount of any future share repurchases and/or dividends, as well as the risks described in Wyndham’s most recent Annual Report on Form 10-K filed with the Securities and Exchange Commission and any subsequent reports filed with the Securities and Exchange Commission. These risks and uncertainties are not the only ones Wyndham may face and additional risks may arise or become material in the future. Wyndham undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, subsequent events or otherwise, except as required by law.

Company Increases Quarterly Dividend by 8% and Provides Full-Year 2025 Outlook

PARSIPPANY, N.J., February 12, 2025 – Wyndham Hotels & Resorts (NYSE: WH) today announced results for the three months and year ended December 31, 2024. Highlights include:

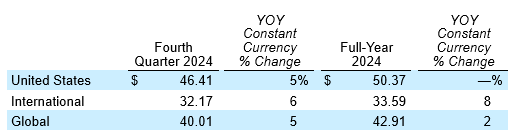

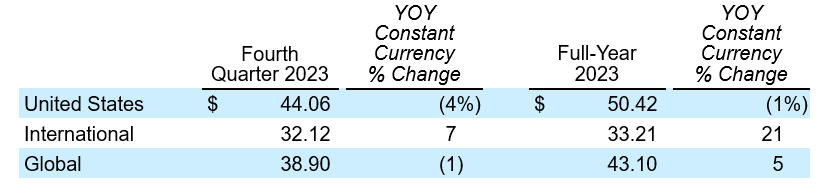

Global RevPAR grew 5% compared to fourth quarter 2023 in constant currency, a 400 basis point improvement sequentially; full-year global RevPAR grew 2% year-over-year in constant currency.

U.S. RevPAR grew 5% compared to fourth quarter 2023, a 600 basis point improvement sequentially; full-year U.S. RevPAR was flat.

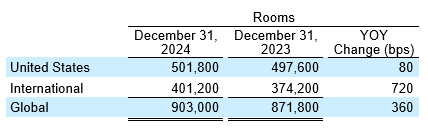

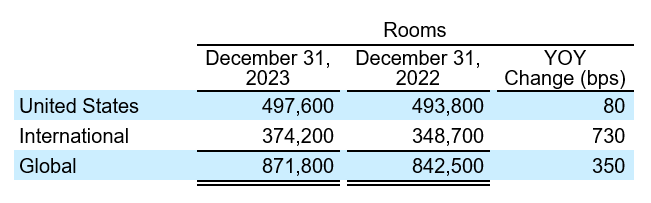

System-wide rooms grew 4% year-over-year.

Opened a record 68,700 rooms globally, representing 4% year-over-year growth, including nearly 28,000 in the U.S., which also grew 4% year-over-year.

Global retention rate reaches record level at 95.7%.

Development pipeline grew 2% sequentially and 5% year-over-year to a record 252,000 rooms.

Fourth quarter diluted earnings per share increased 80% to $1.08 and adjusted diluted EPS grew 14% to $1.04, or approximately 18% on a comparable basis; full-year 2024 diluted earnings per share increased 6% to $3.61 and adjusted diluted EPS grew 8% to $4.33, or approximately 10% on a comparable basis.

Fourth quarter net income increased 70% to $85 million and adjusted net income increased 9% to $82 million, or approximately 13% on a comparable basis; full-year 2024 net income was $289 million, or flat year-over-year, and adjusted net income increased 2% to $347 million, or approximately 4% on a comparable basis.

Fourth quarter adjusted EBITDA increased 9% to $168 million, or approximately 12% on a comparable basis; full-year 2024 adjusted EBITDA increased 5% to $694 million, or approximately 7% on a comparable basis.

Returned $430 million to shareholders for the full-year through $308 million of share repurchases and quarterly cash dividends of $0.38 per share.

Board of Directors recently authorized an 8% increase in the quarterly cash dividend to $0.41 per share beginning with the dividend expected to be declared in the first quarter 2025.

“We’re proud to report a very strong finish to 2024 with net rooms growth of 4% and comparable adjusted EBITDA growth of 7%. Our team’s focus on expanding into higher FeePAR markets, growing our extended-stay footprint and unlocking new ancillary revenue streams underscore the diverse growth opportunities inherent in our asset-light, resilient business model,” said Geoff Ballotti, president and chief executive officer. “What excites us most about our future is the developer interest in, and demand for, our brands both here and overseas, reflected in a pipeline that grew another 5% to a record quarter-of-a-million rooms that will open in the coming years with significant FeePAR premiums compared to our existing system. This, when coupled with improving customer demand we’re seeing across both our leisure and infrastructure segments, lays a solid foundation for sustained momentum and meaningful value creation for our shareholders, guests, franchisees and team members for many years to come.”

System Size and Development

The Company’s global system grew 4%. Importantly, these results included 4% growth in the higher RevPAR midscale and above segments in the U.S. as well as strong growth in the Company’s higher RevPAR EMEA and Latin America regions, which grew a combined 7%. The Company also increased its retention rate by another 10 basis points year-over-year, ending the year at a record 95.7%.

On December 31, 2024, the Company’s global development pipeline consisted of approximately 2,100 hotels and 252,000 rooms, representing another record-high level and a 5% year-over-year increase. Key highlights include:

7% growth in the U.S. and 4% internationally

18th consecutive quarter of sequential pipeline growth

Approximately 70% of the pipeline is in the midscale and above segments, which grew 5% year-over-year

Approximately 17% of the pipeline is in the extended stay segment

Approximately 58% of the pipeline is international

Approximately 78% of the pipeline is new construction and approximately 35% of these projects have broken ground

RevPAR

Fourth quarter global RevPAR increased 5% in constant currency compared to 2023, reflecting 5% growth in the U.S., which accelerated throughout the quarter, and 6% growth internationally. For the full year, global RevPAR was flat compared to 2023 on a reported basis, in line with the Company’s outlook, and grew 2% in constant currency reflecting flat growth in the U.S. and 8% growth internationally.

In the U.S., fourth quarter results included 140 basis points of favorable hurricane impacts; excluding which, RevPAR grew 4% year-over-year reflecting strength in both weekday business bookings and weekend leisure demand. Overall, U.S. RevPAR improved 620 basis points sequentially from third quarter, or 480 basis points excluding hurricane impacts.

Internationally, RevPAR strength was driven by ADR growth of 6% in constant currency, while occupancy remained flat. The Company’s EMEA and Latin America regions saw the largest increases year-over-year in the fourth quarter, collectively growing 15%. RevPAR for the Company’s China region declined 11% in the fourth quarter, driven by a 10% decrease in ADR.

Operating Results

Fourth Quarter

Fee-related and other revenues grew 7% to $341 million compared to $320 million in fourth quarter 2023, which reflects higher royalties and franchise fees.

Net income grew 70% to $85 million compared to $50 million in fourth quarter 2023, reflecting higher adjusted EBITDA, as well as a lower effective tax rate and lower foreign currency impact for highly inflationary countries, which were partially offset by higher interest expense.

Adjusted EBITDA grew 9% to $168 million compared to $154million in fourth quarter 2023. This increase included a $4 million unfavorable impact from expected marketing fund variability, excluding which adjusted EBITDA grew 12% on a comparable basis, primarily reflecting higher royalties and franchise fees and margin expansion.

Diluted earnings per share grew 80% to $1.08 compared to $0.60 in fourth quarter 2023, which primarily reflects higher net income and the benefit of a lower share count due to share repurchase activity.

Adjusted diluted EPS grew 14% to $1.04 compared to $0.91 in fourth quarter 2023. This increase included an unfavorable impact of $0.04 per share related to expected marketing fund variability (after estimated taxes). On a comparable basis, adjusted diluted EPS increased approximately 18% year-over-year reflecting comparable adjusted EBITDA growth and the benefit of share repurchase activity, partially offset by higher interest expense.

During fourth quarter 2024, the Company’s marketing fund revenues exceeded expenses by $5 million; while in fourth quarter 2023, the Company’s marketing fund revenues exceeded expenses by $9 million, resulting in $4 million of marketing fund variability.

Full Year

Fee-related and other revenues grew 1% to $1.40 billion compared to $1.38 billion in full-year 2023, which included $18 million of pass-through revenues associated with the Company’s 2023 global franchisee conference, absent which, fee-related and other revenue increased 3%. This growth primarily reflects higher royalties and franchise fees and ancillary revenues.

The Company reported net income of $289 million, consistent with 2023, as higher adjusted EBITDA was offset by higher transaction-related expenses in connection with defending an unsuccessful hostile takeover attempt. Other items include higher interest expense, restructuring costs and an impairment charge, which were offset by a lower effective tax rate, the absence of foreign currency impacts from highly inflationary countries and a benefit from the reversal of a spin-off related matter.

Adjusted EBITDA grew 5% to $694 million compared to $659million in full-year 2023. This increase included a $10 million unfavorable impact, as expected, from marketing fund variability, excluding which adjusted EBITDA grew 7% on a comparable basis, primarily reflecting higher royalties and franchise fees, increased ancillary revenues and margin expansion.

Diluted earnings per share grew 6% to $3.61 compared to $3.41 in full-year 2023, which primarily reflects the benefit of a lower share count due to share repurchase activity.

Adjusted diluted EPS grew 8% to $4.33 compared to $4.01 in full-year 2023. This increase included an unfavorable impact of $0.09 per share, as expected, related to marketing fund variability (after estimated taxes). On a comparable basis, adjusted diluted EPS increased approximately 10% year-over-year reflecting comparable adjusted EBITDA growth and the benefit of share repurchase activity, partially offset by higher interest expense.

During full-year 2024, the Company’s marketing fund expenses exceeded revenues by $1 million; while in 2023, the Company’s marketing fund revenues exceeded expenses by $9 million, resulting in $10 million of marketing fund variability.

Full reconciliations of GAAP results to the Company’s non-GAAP adjusted measures for all reported periods appear in the tables to this press release.

Balance Sheet and Liquidity

The Company generated $290 million of net cash provided by operating activities and $397 million of adjusted free cash flow in full-year 2024. The Company ended the quarter with a cash balance of $103 million and approximately $765 million in total liquidity.

The Company’s net debt leverage ratio was 3.4 times at December 31, 2024, just below the midpoint of the Company’s 3 to 4 times stated target range and in line with expectations.

Share Repurchases and Dividends

During the fourth quarter, the Company repurchased approximately 0.3 million shares of its common stock for $23 million. For the full-year 2024, the Company repurchased approximately 4.1 million shares of its common stock for $308 million.

The Company paid common stock dividends of $30 million, or $0.38 per share, during the fourth quarter 2024 for a total of $122 million, or $1.52 per share, for the full-year 2024.

For the full-year 2024, the Company returned $430 million to shareholders through share repurchases and quarterly cash dividends.

The Company’s Board of Directors authorized an 8% increase in the quarterly cash dividend to $0.41 per share, beginning with the dividend expected to be declared in first quarter 2025.

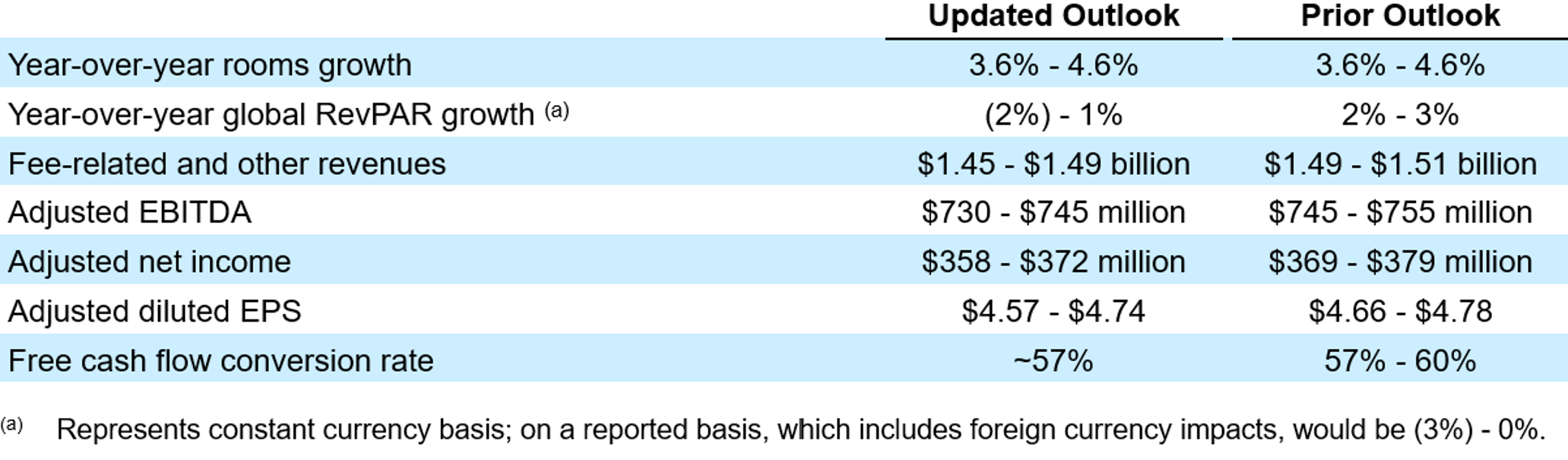

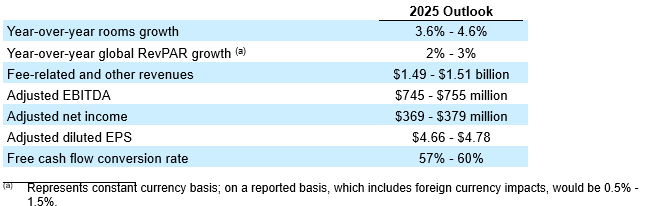

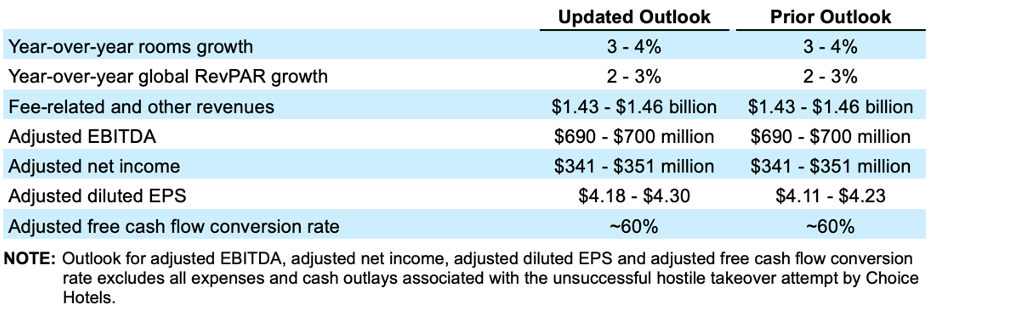

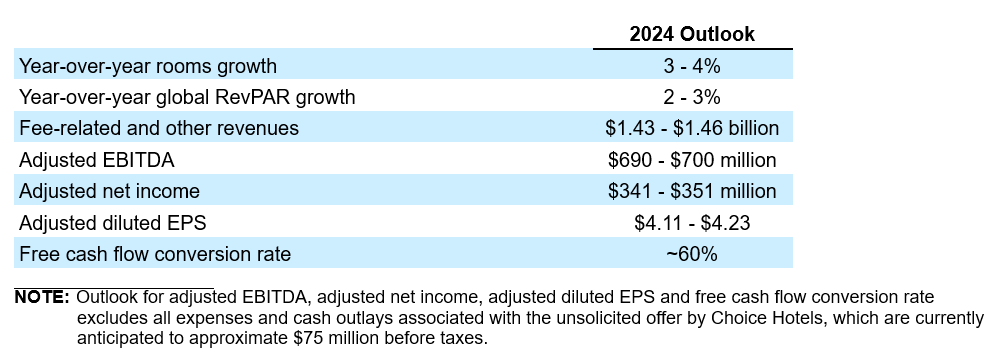

Outlook

The Company provided the following outlook for full-year 2025:

The Company continues to expect marketing fund revenues to equal expenses during full-year 2025 though seasonality of spend will affect the quarterly comparisons throughout the year.

More detailed projections are available in Table 8 of this press release. The Company is providing certain financial metrics only on a non-GAAP basis because, without unreasonable efforts, it is unable to predict with reasonable certainty the occurrence or amount of all of the adjustments or other potential adjustments that may arise in the future during the forward-looking period, which can be dependent on future events that may not be reliably predicted. Based on past reported results, where one or more of these items have been applicable, such excluded items could be material, individually or in the aggregate, to the reported results.

Conference Call Information

Wyndham Hotels will hold a conference call with investors to discuss the Company’s results and outlook on Thursday, February 13, 2025 at 8:30 a.m. ET. Listeners can access the webcast live through the Company’s website at https://investor.wyndhamhotels.com. The conference call may also be accessed by dialing 800 225-9448 and providing the passcode “Wyndham”. Listeners are urged to call at least five minutes prior to the scheduled start time. An archive of this webcast will be available on the website beginning at noon ET on February 13, 2025. A telephone replay will be available for approximately ten days beginning at noon ET on February 13, 2025 at 800 839-5127.

Presentation of Financial Information

Financial information discussed in this press release includes non-GAAP measures, which include or exclude certain items. These non-GAAP measures differ from reported GAAP results and are intended to illustrate what management believes are relevant period-over-period comparisons and are helpful to investors as an additional tool for further understanding and assessing the Company’s ongoing operating performance. The Company uses these measures internally to assess its operating performance, both absolutely and in comparison to other companies, and to make day to day operating decisions, including in the evaluation of selected compensation decisions. Exclusion of items in the Company’s non-GAAP presentation should not be considered an inference that these items are unusual, infrequent or non-recurring. Full reconciliations of GAAP results to the comparable non-GAAP measures for the reported periods appear in the financial tables section of this press release.

About Wyndham Hotels & Resorts

Wyndham Hotels & Resorts (NYSE: WH) is the world’s largest hotel franchising company by the number of franchised properties, with approximately 9,300 hotels across over 95 countries on six continents. Through its network of approximately 903,000 rooms appealing to the everyday traveler, Wyndham commands a leading presence in the economy and midscale segments of the lodging industry. The Company operates a portfolio of 25 hotel brands, including Super 8®, Days Inn®, Ramada®, Microtel®, La Quinta®, Baymont®, Wingate®, AmericInn®, ECHO Suites®, Registry Collection Hotels®, Trademark Collection® and Wyndham®. The Company’s award-winning Wyndham Rewards loyalty program offers approximately 114 million enrolled members the opportunity to redeem points at thousands of hotels, vacation club resorts and vacation rentals globally. For more information, visit https://investor.wyndhamhotels.com. The Company may use its website and social media channels as means of disclosing material non-public information and for complying with its disclosure obligations under Regulation FD. Disclosures of this nature will be included on the Company’s website in the Investors section, which can currently be accessed at https://investor.wyndhamhotels.com or on the Company’s social media channels, including the Company’s LinkedIn account which can currently be accessed at https://www.linkedin.com/company/wyndhamhotels. Accordingly, investors should monitor this section of the Company’s website and the Company’s social media channels in addition to following the Company’s press releases, filings submitted with the Securities and Exchange Commission and any public conference calls or webcasts.

Forward-Looking Statements

This press release contains “forward-looking statements” within the meaning of the federal securities laws, including statements related to Wyndham’s current views and expectations with respect to its future performance and operations, including revenues, earnings, cash flow and other financial and operating measures, share repurchases and dividends and restructuring charges. Forward-looking statements are any statements other than statements of historical fact, including those that convey management’s expectations as to the future based on plans, estimates and projections at the time Wyndham makes the statements and may be identified by words such as “will,” “expect,” “believe,” “plan,” “anticipate,” “predict,” “intend,” “goal,” “future,” “forward,” “remain,” “confident,” “outlook,” “guidance,” “target,” “objective,” “estimate,” “projection” and similar words or expressions, including the negative version of such words and expressions. Such forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause the actual results, performance or achievements of Wyndham to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press release.

Factors that could cause actual results to differ materially from those in the forward-looking statements include, without limitation, general economic conditions, including inflation, higher interest rates and potential recessionary pressures; the performance of the financial and credit markets; the economic environment for the hospitality industry; operating risks associated with the hotel franchising business; Wyndham’s relationships with franchisees; the impact of war, terrorist activity, political instability or political strife, including the ongoing conflicts between Russia and Ukraine and conflicts in the Middle East, respectively; global or regional health crises or pandemics including the resulting impact on Wyndham’s business, operations, financial results, cash flows and liquidity, as well as the impact on its franchisees, guests and team members, the hospitality industry and overall demand for and restrictions on travel; Wyndham’s ability to satisfy obligations and agreements under its outstanding indebtedness, including the payment of principal and interest and compliance with the covenants thereunder; risks related to Wyndham’s ability to obtain financing and the terms of such financing, including access to liquidity and capital; and Wyndham’s ability to make or pay, plans for and the timing and amount of any future share repurchases and/or dividends, as well as the risks described in Wyndham’s most recent Annual Report on Form 10-K filed with the Securities and Exchange Commission and any subsequent reports filed with the Securities and Exchange Commission. These risks and uncertainties are not the only ones Wyndham may face and additional risks may arise or become material in the future. Wyndham undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, subsequent events or otherwise, except as required by law.

Company Raises Full-Year 2024 EPS Outlook and Reaffirms Remaining Outlook

Grows System Size by 4% and Development Pipeline by 5%

PARSIPPANY, N.J., October 23, 2024 – Wyndham Hotels & Resorts (NYSE: WH) today announced results for the three months ended September 30, 2024. Highlights include:

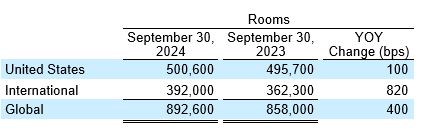

System-wide rooms grew 4% year-over-year.

Opened over 17,000 rooms globally, including nearly 7,000 in the U.S., which increased 15% year-over-year, and the second ECHO Suites Extended Stay by Wyndham.

Awarded 197 development contracts globally, including 95 contracts in the U.S., which increased 10% year-over-year.

Development pipeline grew 1% sequentially and 5% year-over-year to a record 248,000 rooms.

Global RevPAR grew 1% in constant currency.

Ancillary revenues increased 8% compared to third quarter 2023.

Diluted earnings per share increased 7%, to $1.29, and adjusted diluted EPS grew 6%, to $1.39, or approximately 10% on a comparable basis.

Net income was $102 million for the third quarter, a 1% decrease over the prior-year quarter; adjusted net income was $110 million, a 1% decrease over the prior-year quarter, or a 3% increase on a comparable basis.

Adjusted EBITDA increased 4% compared with the prior-year quarter, to $208 million, or 7% on a comparable basis.

Returned $126 million to shareholders through $97 million of share repurchases and quarterly cash dividends of $0.38 per share.

“Our teams around the world once again delivered exceptional results, executing our long-term growth strategy and achieving 7% growth in comparable adjusted EBITDA fueled by continued system expansion, higher royalty rates and growth in our ancillary revenues,” said Geoff Ballotti, president and chief executive officer. “We awarded 10% more franchise contracts domestically this quarter, driving 5% growth in our development pipeline. Stabilizing RevPAR trends and improving comparisons coupled with increased infrastructure demand are expected to pave the way for improved results in the coming quarters. We remain steadfast in our long-term strategy, aimed at delivering outstanding value to our guests, franchisees and shareholders to whom we’ve returned nearly $380 million year-to-date in the form of dividends and share repurchases.”

System Size and Development

The Company’s global system grew 4%, reflecting 1% growth in the U.S. and 8% internationally. As expected, these increases included 3% growth in the higher RevPAR midscale and above segments in the U.S., as well as strong growth in the Company’s EMEA and Latin America regions, which each grew 11%. The Company continued to improve its retention rate and remains solidly on track to achieve its net room growth outlook of 3 to 4% for the full year 2024.

On September 30, 2024, the Company’s global development pipeline consisted of approximately 2,100 hotels and 248,000 rooms, representing another record-high level and a 5% year-over-year increase. Key highlights include:

7% growth in the U.S. and 3% internationally

17th consecutive quarter of sequential pipeline growth

Approximately 70% of the pipeline is in the midscale and above segments, which grew 6% year-over-year

Approximately 14% of the pipeline represents ECHO Suites Extended Stay by Wyndham for which the Company has awarded a total of 283 contracts since its launch.

Approximately 58% of the pipeline is international

Approximately 79% of the pipeline is new construction and approximately 35% of these projects have broken ground

During the third quarter of 2024, the Company awarded 197 new contracts, including 95 contracts in the U.S., which increased 10% year-over-year.

RevPAR

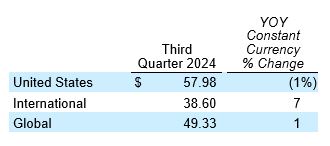

Third quarter global RevPAR increased 1% in constant currency compared to 2023, reflecting a 1% decline in the U.S. and 7% growth internationally.

In the U.S., RevPAR for the Company’s midscale and above segments was unchanged year-over-year while RevPAR for its economy segment declined 2% reflecting a modest acceleration from the second quarter with a sequential improvement of 10 basis points. Additionally, the Company’s U.S. economy brands continued to strengthen their position, gaining 50 basis points of market share in the third quarter driven by performance in oil and gas markets, which grew 250 basis points in the quarter, and in the five states with the highest infrastructure bill spend, which collectively grew 80 basis points. U.S. occupancy remained consistent, highlighting the resilience of the select-service space and consumer demand for these products.

Internationally, RevPAR for the Company’s EMEA, Latin America and Canada regions collectively increased 13% due to both continued pricing power, with ADR up 11%, and occupancy growth of 2%. RevPAR for the Company’s APAC region declined 7% driven by a 2% decrease in occupancy and a 5% decrease in ADR. Importantly, the third quarter RevPAR performance for APAC represented a 500 basis point sequential improvement.

Third Quarter Operating Results

Fee-related and other revenues were $394 million compared to $400 million in third quarter 2023, which included $18 million of pass-through revenues associated with the Company’s 2023 global franchisee conference, absent which, fee-related and other revenue increased 3%. The growth in fee-related and other revenues reflects higher royalties and franchise fees and ancillary revenues.

The Company generated net income of $102 million compared to $103 million in third quarter 2023. The decrease was primarily reflective of higher interest expense, partially offset by higher adjusted EBITDA.

Adjusted EBITDA grew 4% to $208 million compared to $200million in third quarter 2023. This increase included a $5 million unfavorable impact from marketing fund variability, excluding which adjusted EBITDA grew 7% on a comparable basis, primarily reflecting higher royalties and franchise fees, increased ancillary revenues and margin expansion.

Diluted earnings per share was $1.29 compared to $1.21 in third quarter 2023. This increase primarily reflects the benefit of a lower share count due to share repurchase activity.

Adjusted diluted EPS grew 6% to $1.39 compared to $1.31 in third quarter 2023. This increase included an unfavorable impact of $0.04 per share related to expected marketing fund variability (after estimated taxes). On a comparable basis, adjusted diluted EPS increased approximately 10% year-over-year reflecting comparable adjusted EBITDA growth and the benefit of share repurchase activity, partially offset by higher interest expense.

During third quarter 2024, the Company’s marketing fund revenues exceeded expenses by $12 million, in line with expectations; while in third quarter 2023, the Company’s marketing fund revenues exceeded expenses by $17 million, resulting in $5 million of marketing fund variability. The Company continues to expect marketing fund revenues to roughly equal expenses during full-year 2024.

Full reconciliations of GAAP results to the Company’s non-GAAP adjusted measures for all reported periods appear in the tables to this press release.

Balance Sheet and Liquidity

The Company generated $79 million of net cash provided by operating activities and $96 million of adjusted free cash flow in third quarter 2024. The Company ended the quarter with a cash balance of $72 million and approximately $750 million in total liquidity.

The Company’s net debt leverage ratio was 3.5 times at September 30, 2024, the midpoint of the Company’s 3 to 4 times stated target range.

During the third quarter of 2024, the Company executed $350 million of new interest rate swaps on its Term Loan B Facility, which will expire in 2028. The fixed rate of the new swaps is 3.3%. As a result, the Company ended the third quarter with approximately 80% of its total debt at a fixed rate and 20% variable.

Share Repurchases and Dividends

During the third quarter, the Company repurchased approximately 1.3 million shares of its common stock for $97 million. Year-to-date through September 30, the Company repurchased approximately 3.8 million shares of its common stock for $285 million.

The Company paid common stock dividends of $29 million, or $0.38 per share, during the third quarter 2024 and $92 million, or $1.14 per share, year-to-date.

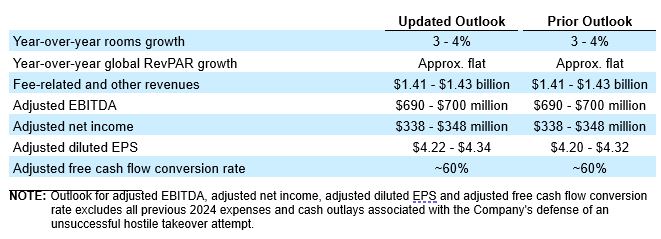

Full-Year 2024 Outlook

The Company is refining its outlook as follows:

Year-over-year growth rates for adjusted EBITDA, adjusted net income and adjusted diluted EPS are not comparable due to full-year 2023 marketing fund revenues exceeding expenses by $9 million, which substantially completed the recovery of the $49 million support the Company provided to its owners during COVID. The Company continues to expect marketing fund revenues to equal expenses during full-year 2024 though seasonality of spend will affect the quarterly comparisons throughout the year.

More detailed projections are available in Table 8 of this press release. The Company is providing certain financial metrics only on a non-GAAP basis because, without unreasonable efforts, it is unable to predict with reasonable certainty the occurrence or amount of all of the adjustments or other potential adjustments that may arise in the future during the forward-looking period, which can be dependent on future events that may not be reliably predicted. Based on past reported results, where one or more of these items have been applicable, such excluded items could be material, individually or in the aggregate, to the reported results.

Conference Call Information

Wyndham Hotels will hold a conference call with investors to discuss the Company’s results and outlook on Thursday, October 24, 2024 at 8:30 a.m. ET. Listeners can access the webcast live through the Company’s website at https://investor.wyndhamhotels.com. The conference call may also be accessed by dialing 800 579-2543 and providing the passcode “Wyndham”. Listeners are urged to call at least five minutes prior to the scheduled start time. An archive of this webcast will be available on the website beginning at noon ET on October 24, 2024. A telephone replay will be available for approximately ten days beginning at noon ET on October 24, 2024 at 800 695-0715.

Presentation of Financial Information

Financial information discussed in this press release includes non-GAAP measures, which include or exclude certain items. These non-GAAP measures differ from reported GAAP results and are intended to illustrate what management believes are relevant period-over-period comparisons and are helpful to investors as an additional tool for further understanding and assessing the Company’s ongoing operating performance. The Company uses these measures internally to assess its operating performance, both absolutely and in comparison to other companies, and to make day to day operating decisions, including in the evaluation of selected compensation decisions. Exclusion of items in the Company’s non-GAAP presentation should not be considered an inference that these items are unusual, infrequent or non-recurring. Full reconciliations of GAAP results to the comparable non-GAAP measures for the reported periods appear in the financial tables section of this press release.

About Wyndham Hotels & Resorts

Wyndham Hotels & Resorts (NYSE: WH) is the world’s largest hotel franchising company by the number of properties, with approximately 9,200 hotels across over 95 countries on six continents. Through its network of approximately 893,000 rooms appealing to the everyday traveler, Wyndham commands a leading presence in the economy and midscale segments of the lodging industry. The Company operates a portfolio of 25 hotel brands, including Super 8®, Days Inn®, Ramada®, Microtel®, La Quinta®, Baymont®, Wingate®, AmericInn®, Hawthorn Suites®, Trademark Collection® and Wyndham®. The Company’s award-winning Wyndham Rewards loyalty program offers approximately 112 million enrolled members the opportunity to redeem points at thousands of hotels, vacation club resorts and vacation rentals globally. For more information, visit https://investor.wyndhamhotels.com. The Company may use its website and social media channels as means of disclosing material non-public information and for complying with its disclosure obligations under Regulation FD. Disclosures of this nature will be included on the Company’s website in the Investors section, which can currently be accessed at https://investor.wyndhamhotels.com or on the Company’s social media channels, including the Company’s LinkedIn account which can currently be accessed at https://www.linkedin.com/company/wyndhamhotels. Accordingly, investors should monitor this section of the Company’s website and the Company’s social media channels in addition to following the Company’s press releases, filings submitted with the Securities and Exchange Commission and any public conference calls or webcasts.

Forward-Looking Statements