Wyndham Hotels & Resorts Reports Strong First Quarter Results

Company Grows System Size by 4% and Development Pipeline to Record 2,200 Hotels

U.S. RevPAR Recovery Ahead of Expectations

PARSIPPANY, N.J., April 29, 2026 – Wyndham Hotels & Resorts (NYSE: WH) today announced results for the three months ended March 31, 2026. Highlights include:

- System-wide rooms grew 4% year-over-year.

- Awarded development contracts in the U.S. increased 8% year-over-year.

- Development pipeline grew 3% year-over-year to a record of over 259,000 rooms and over 2,200 hotels.

- S. RevPAR was flat year-over-year, 250 basis points ahead of midpoint of expectations.

- Ancillary revenues increased 21% year-over-year.

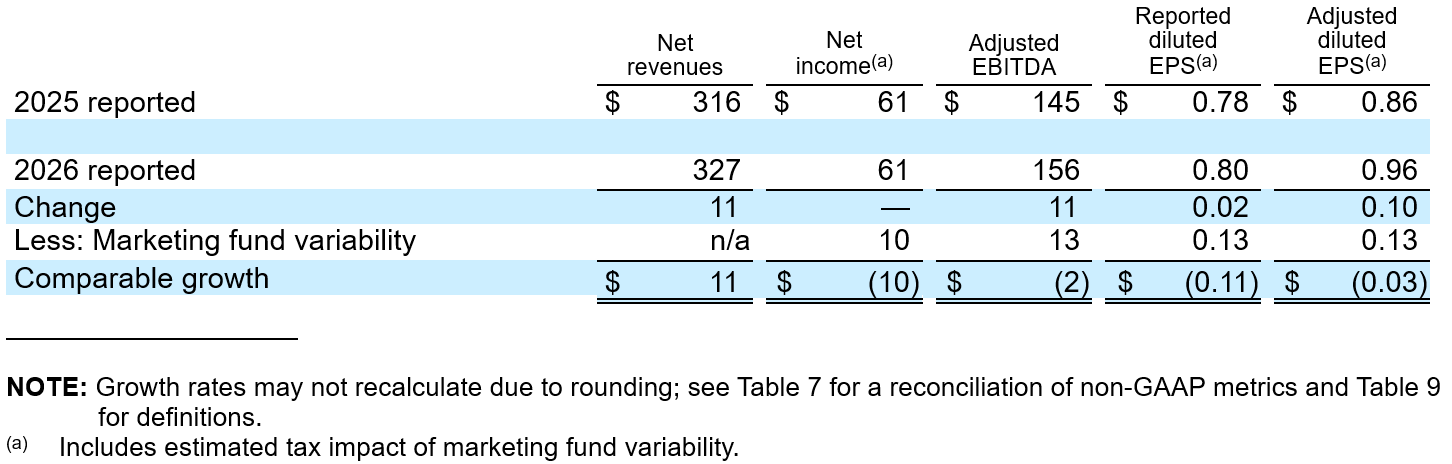

- Net income remained flat year-over-year at $61 million; adjusted net income increased 9% year-over-year to $73 million, or 6% lower on a comparable basis.

- Diluted earnings per share grew 3% to $0.80 from $0.78 in the prior-year quarter and adjusted diluted EPS grew 12% year-over-year to $0.96, or 3% lower on a comparable basis.

- Adjusted EBITDA increased 8% year-over-year to $156 million, or 1% lower on a comparable basis.

- Net cash provided by operating activities of $42 million and free cash flow of $64

- Returned $85 million to shareholders through $51 million of share repurchases and quarterly cash dividends of $0.43 per share.

- Issued $650 million aggregate principal amount of 5.625% senior unsecured notes, due 2033, the net proceeds of which were primarily used to fully repay then-outstanding revolver and term loan A borrowings.

“We delivered a strong start to the year, highlighted by record-level first-quarter openings and a continued expansion of our development pipeline,” said Geoff Ballotti, president and chief executive officer. “As U.S. RevPAR in our economy and midscale segments continues to recover ahead of expectations, we approach the peak leisure summer season with increasing optimism. We’ve never been more confident in our ability to drive sustained long-term value creation for franchisees, guests and shareholders by adding high-quality, FeePAR-accretive hotels to our portfolio, growing ancillary revenues and scaling AI to further differentiate our industry-leading technology platform.”

System Size and Development

The Company’s global system grew 4%, including flat growth in the U.S., which includes the impact from the loss of legacy affiliated rooms, 12% direct-franchised growth in the Company’s Asia Pacific region and 9% growth in the Company’s higher RevPAR EMEA and Latin America regions.

As of March 31, 2026, the Company’s global development pipeline increased 3% vs. prior-year to a record-high level of over 259,000 rooms and over 2,200 hotels. Key highlights include:

- 3% pipeline growth in the U.S. and 2% growth internationally

- Approximately 70% of the pipeline is in the midscale and above segments

- Approximately 17% of the pipeline is in the extended stay segment

- Approximately 43% of the pipeline is in the U.S.

- Approximately 77% of the pipeline is new construction and approximately 35% of these projects have broken ground; rooms under construction grew 3% year-over-year

RevPAR

First quarter global RevPAR decreased 1% in constant currency compared to 2025, reflecting flat performance in the U.S. and a 1% decline internationally.

In the U.S., the year-over-year comparison was impacted by approximately 40 basis points of unfavorable hurricane impacts related to first quarter 2025; excluding which, RevPAR increased over 600 basis points sequentially and approximately 10 basis points year-over-year reflecting stabilized occupancy and ADR levels. Continued strength across the Midwest and growth in Texas was partially offset by performance in Florida and California, which both improved sequentially yet declined year-over-year.

Internationally, constant currency growth of 8% in Canada reflected significant pricing power and continued demand growth, while growth of 5% in Southeast Asia and the Pacific Rim and 1% in EMEA each primarily reflected improved demand. The growth in those regions was more than offset by softness in China where RevPAR improved over 500 basis points sequentially, yet declined 5% year-over-year, and Latin America, which declined 4% year-over-year primarily due to lower U.S. cross-border demand in Mexico.

Operating Results

The comparability of the Company’s first quarter results is impacted by marketing fund variability. The Company’s reported results and comparable-basis results (adjusted to neutralize these impacts) are presented below to enhance transparency and provide a better understanding of the results of the Company’s ongoing operations.

- Net revenues grew 3% to $327 million compared to $316 million in the first quarter of 2025, reflecting a 21% increase in ancillary revenues and global net room growth of 4%, partially offset by lower other franchise fees and the deferral of fees from Revo Hospitality Group (“Revo”).

- Net income remained flat at $61 million compared to the first quarter of 2025, primarily reflecting higher adjusted EBITDA offset by restructuring and other-related costs, as well as transaction-related costs resulting from the Company’s issuance of 5.625% senior unsecured notes. Adjusted net income grew 9% to $73 million compared to $67 million in the first quarter of 2025.

- Adjusted EBITDA increased 8% to $156 million compared to $145million in the first quarter of 2025. This increase included a $13 million favorable impact from marketing fund variability, excluding which adjusted EBITDA declined 1% on a comparable basis. This decline primarily reflects lower royalties and franchise fees and the absence of one-time cost reductions, partially offset by increased ancillary revenues.

- Diluted EPS grew 3% to $80 compared to $0.78 in the first quarter of 2025, which primarily reflects the benefit of a lower share count due to share repurchase activity.

- Adjusted diluted EPS increased 12% to $0.96 compared to $0.86 in the first quarter of 2025. This increase included a favorable impact of $13 per share related to marketing fund variability (after estimated taxes). On a comparable basis, adjusted diluted EPS decreased approximately 3% year-over-year primarily reflecting a comparable basis decline in adjusted EBITDA, a marginally higher effective tax rate and increased interest expense, partially offset by the benefit of share repurchase activity.

Full reconciliations of GAAP results to the Company’s non-GAAP adjusted measures for all reported periods appear in the tables to this press release.

Balance Sheet and Liquidity

The Company generated $42 million of net cash provided by operating activities and $64 million of free cash flow in the first quarter 2026. The Company ended the quarter with a cash balance of $79 million and $1.1 billion in total liquidity, which includes the effect of the February 2026 issuance of $650 million aggregate principal amount of senior unsecured notes bearing interest at 5.625%. The net proceeds from the issuance were primarily used to fully repay then-outstanding revolver and term loan A borrowings.

The Company’s net debt leverage ratio was 3.5 times at March 31, 2026, at the midpoint of the Company’s 3 to 4 times stated target range and in line with expectations.

Share Repurchases and Dividends

During the first quarter, the Company repurchased approximately 656,000 shares of its common stock for $51 million.

The Company paid common stock dividends of $34 million, or $0.43 per share, during the first quarter 2026.

Revo Update

As part of the Company’s efforts to pursue all available remedies related to Revo’s ongoing insolvency proceedings and optimize the recoverability for the Company’s shareholders, the Company exercised its rights to foreclose on and take ownership of two properties in Europe. The Company expects these properties to generate approximately $10 million of net revenues in full-year 2026 with a limited impact to earnings as the Company works to stabilize operations and implement an asset management plan to maximize value.

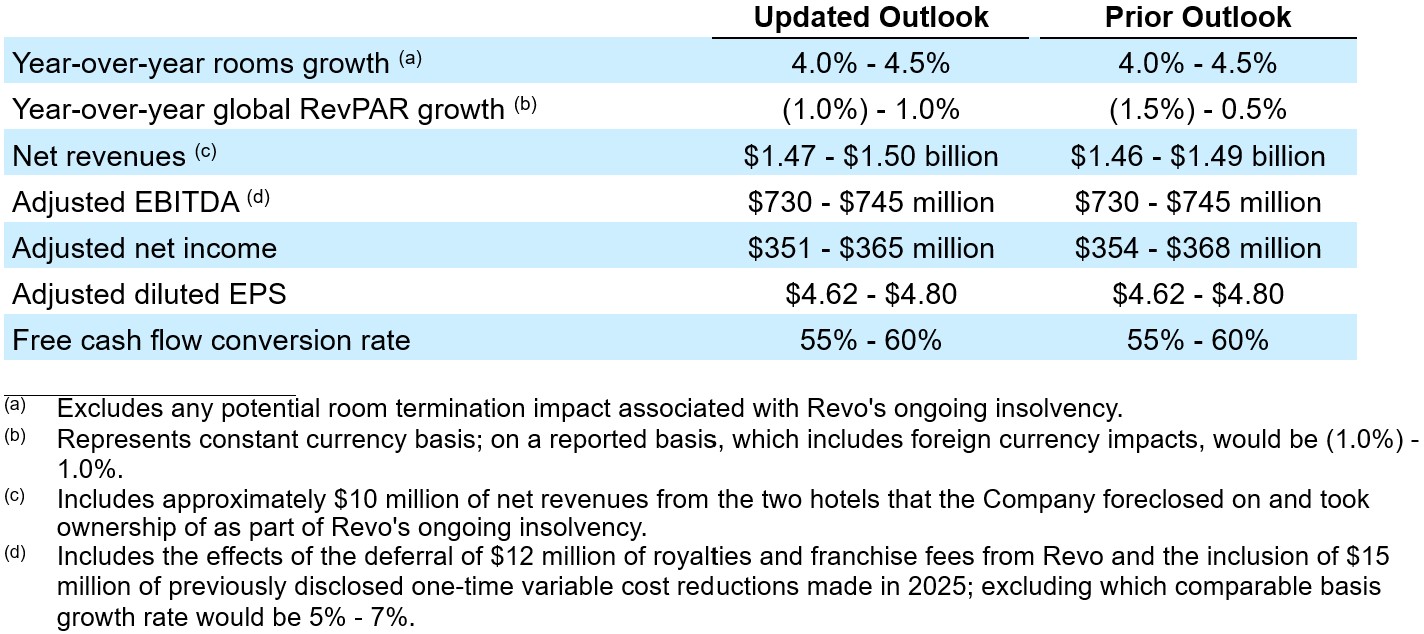

Outlook

The Company is updating its full-year outlook as follows:

The Company expects marketing fund revenues to roughly equal expenses during full-year 2026 though seasonality of spend will affect the quarterly comparisons throughout the year.

More detailed projections are available in Table 8 of this press release. The Company is providing certain financial metrics only on a non-GAAP basis because, without unreasonable efforts, it is unable to predict with reasonable certainty the occurrence or amount of all of the adjustments or other potential adjustments that may arise in the future during the forward-looking period, which can be dependent on future events that may not be reliably predicted. Based on past reported results, where one or more of these items have been applicable, such excluded items could be material, individually or in the aggregate, to the reported results.

Conference Call Information

Wyndham Hotels will hold a conference call with investors to discuss the Company’s results and outlook on Thursday, April 30, 2026 at 8:30 a.m. ET. Listeners can access the webcast live through the Company’s website at https://investor.wyndhamhotels.com. The conference call may also be accessed by dialing 800 343-4136 and providing the passcode “Wyndham”. Listeners are urged to call at least five minutes prior to the scheduled start time. An archive of this webcast will be available on the website beginning at noon ET on April 30, 2026. A telephone replay will be available for approximately ten days beginning at noon ET on April 30, 2026 at 800 695-0715.

Presentation of Financial Information

Financial information discussed in this press release includes non-GAAP measures, which include or exclude certain items. These non-GAAP measures differ from reported GAAP results and are intended to illustrate what management believes are relevant period-over-period comparisons and are helpful to investors as an additional tool for further understanding and assessing the Company’s ongoing operating performance. The Company uses these measures internally to assess its operating performance, both absolutely and in comparison to other companies, and to make day to day operating decisions, including in the evaluation of selected compensation decisions. Exclusion of items in the Company’s non-GAAP presentation should not be considered an inference that these items are unusual, infrequent or non-recurring. Full reconciliations of GAAP results to the comparable non-GAAP measures for the reported periods appear in the financial tables section of this press release.

About Wyndham Hotels & Resorts

Wyndham Hotels & Resorts (NYSE: WH) is one of the world’s largest hotel franchising companies with approximately 8,400 hotels across approximately 100 countries on six continents. Through its network of approximately 869,000 franchised and affiliated rooms appealing to the everyday traveler, Wyndham commands a leading presence in the economy and midscale segments of the lodging industry. The Company operates a portfolio of 25 hotel brands, including Super 8®, Days Inn®, Ramada®, Microtel®, La Quinta®, Baymont®, Wingate®, AmericInn®, ECHO Suites®, Registry Collection Hotels®, Trademark Collection® and Wyndham®. The Company’s award-winning Wyndham Rewards loyalty program offers over 124 million enrolled members the opportunity to redeem points at thousands of hotels, vacation club resorts and vacation rentals globally. For more information, visit https://investor.wyndhamhotels.com. The Company may use its website and social media channels as means of disclosing material non-public information and for complying with its disclosure obligations under Regulation FD. Disclosures of this nature will be included on the Company’s website in the Investors section, which can currently be accessed at https://investor.wyndhamhotels.com or on the Company’s social media channels, including the Company’s LinkedIn account which can currently be accessed at https://www.linkedin.com/company/wyndhamhotels. Accordingly, investors should monitor this section of the Company’s website and the Company’s social media channels in addition to following the Company’s press releases, filings submitted with the Securities and Exchange Commission and any public conference calls or webcasts.

Forward-Looking Statements

This press release contains “forward-looking statements” within the meaning of the federal securities laws, including statements related to Wyndham’s current views and expectations with respect to its future performance and operations, including revenues, earnings, cash flow and other financial and operating measures, share repurchases and dividends and restructuring charges. Forward-looking statements are any statements other than statements of historical fact, including those that convey management’s expectations as to the future based on plans, estimates and projections at the time Wyndham makes the statements and may be identified by words such as “will,” “expect,” “believe,” “plan,” “anticipate,” “predict,” “intend,” “goal,” “future,” “forward,” “remain,” “confident,” “outlook,” “guidance,” “target,” “objective,” “estimate,” “projection” and similar words or expressions, including the negative version of such words and expressions. Such forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause the actual results, performance or achievements of Wyndham to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press release.

Factors that could cause actual results to differ materially from those in the forward-looking statements include, without limitation, general economic conditions, including inflation, higher interest rates and potential recessionary pressures, which may impact decisions by consumers and businesses to use travel accommodations; global trade disputes, including with China; the performance of the financial and credit markets; the economic environment for the hospitality industry; operating risks associated with the hotel franchising business; Wyndham’s relationships with franchisees; the ability of franchisees to pay back loans owed to Wyndham; the impact of prior or any future impairment charges related to the credit Wyndham extends to its franchisees; the impact of war, terrorist activity, political instability or political strife; global or regional health crises or pandemics including the resulting impact on Wyndham’s business, operations, financial results, cash flows and liquidity, as well as the impact on its franchisees, guests and team members, the hospitality industry and overall demand for and restrictions on travel; Wyndham’s ability to satisfy obligations and agreements under its outstanding indebtedness, including the payment of principal and interest and compliance with the covenants thereunder; risks related to Wyndham’s ability to obtain financing and the terms of such financing, including access to liquidity and capital; and Wyndham’s ability to make or pay, plans for and the timing and amount of any future share repurchases and/or dividends, as well as the risks described in Wyndham’s most recent Annual Report on Form 10-K filed with the Securities and Exchange Commission and any subsequent reports filed with the Securities and Exchange Commission. These risks and uncertainties are not the only ones Wyndham may face and additional risks may arise or become material in the future. Wyndham undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, subsequent events or otherwise, except as required by law.